If you happen to:

- Get a locked bank account notice?

- Wonder: “Can a bank freeze my account without warning?”

The truth is, yes, they can. No matter where you open your personal or corporate bank account (in Singapore, Hong Kong, Canada, the U.S). Frozen accounts are more common than you think.

Here is a typical case from one of our clients.

Their seized bank account came as a shock. They weren’t sure why it happened or how to get their funds back.

So why would a bank freeze your account in the first place? And more importantly, how do you fix it quickly (and avoid it happening again)?

In this guide, you’ll learn:

- The 7 most common reasons behind a frozen bank account (The eighth reason is the most rare);

- What steps should you take immediately when your account is locked;

- How to prevent your bank account from being seized in the future;

Let’s start with a concrete understanding of what a frozen account is.

1. What is a frozen bank account?

A frozen bank account, or commonly known as a seized account, locked account, or limited account, is an account where your money is locked, and you can’t move it.

A person with a frozen account can not

- Make transfers;

- Withdraw cash (online or ATM);

- Pay bills (Even scheduled payments get stopped;

Account holders can still log in, check their balance, and monitor activity, but they cannot receive or send money via their banking apps.

2. What types of accounts can be frozen?

Any account can be locked, from business bank accounts, personal bank accounts, to joint accounts and checking accounts. Some funds (Social Security benefits, disability payments, retirement funds, unemployment compensation, veterans' benefits, and child support) are exempt from freezing.

3. Do banks announce why they freeze your accounts?

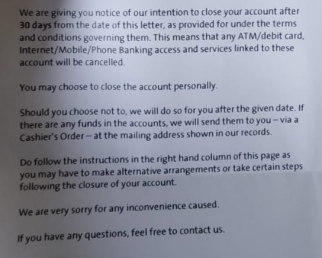

The majority of banks will not announce why they freeze your accounts. In some scenarios, they will send a generic notice (“Account frozen due to security protocols”) to your accounts (Gmail, app notifications) or via phisical letter of notice.

Account shutdown notice from banks

Account shutdown notice from banks

It is your responsibility to check your bank activities and understand why banks put your account on hold.

- What triggered the account freezing;

- What can you do to resolve the problems.

In this guide, our banking experts will show you 7 common reasons why your account is locked and how to resolve.

4. The 7 most common reasons behind a frozen bank account (+ resolutions for each)

| Types of account freeze | What to do |

| High-risk freezes |

|

| Unusual transaction freezes |

|

| Debt-related freezes |

|

| Non-compliance freezes |

|

| Dormancy freezes |

|

| Business liquidation freezes |

|

| Regulatory or legal investigation freeze |

|

4.1. High-risk freezes

Examples of high-risk account freezes

The most common reason banks freeze accounts is suspicious activity that is high-risk.

This doesn’t always mean wrongdoing of the account holder. It is the automatic safeguard protocol of the banks against money laundering, terrorism financing, or fraud.

That is why even legitimate businesses can get flagged if their transactions look unusual.

Here are 5 common high-risk, suspicious activities you may do to activate account freezing:

- Large or sudden deposits/withdrawals (especially cross-border).

- Transfers to or from high-risk countries.(North Korea, Iran, and Myanmar.)

- A sudden spike in transaction volume or frequency. (You typically earn 3,000 USD per month, but you earn 300,000 USD this April)

- Frequent cash deposits (3 to 4 times higher than your normal transactions)

- Buying high-risk assets (gold, diamond, land)

- Transactions that don’t match your business’s normal profile. (Buying toxic chemicals, but your company specializes in fish product exportation)

In summary, if your account/business account performs differently from your normal day-to-day activities, it is more likely to be locked. Because your accounts show signs of being in an anti-money laundering scheme.

How to resolve high-risk freezes

Banks are legally obligated to report red flags. In the US, they file reports with FinCEN. In the UK, it’s the NCA. In Hong Kong, the JFIU.

That’s why suspicious activity freezes are some of the hardest to resolve.

In this situation, the account holder must prove the source and purpose of the funds with legitimate financial transactions and documents to prove the money is for legitimate business activities.

You must go directly to the bank to speak with the banker and bring the relevant documents to resolve this issue. You can not do it via Gmail, telephone calls.

To avoid the high-risk freezes, you should:

- Monitor your transactions monthly so you spot unusual patterns before the bank does.

- Flag high-risk behaviors (like big cross-border transfers) and prepare documentation.

- Notify your bank in advance of large purchases, travel, or transactions outside your normal activity (You can notify your account manager).

4.2. Unusual transaction freezes

Examples of unusual transaction freezes

While similar to suspicious activity, this freeze is more about protecting you from fraud than assuming you’re doing something illegal.

Many freezes of this type are triggered by stolen cards or compromised account credentials.

Sometimes, account freezes occur because high-volume business transactions are mixed with low personal spending when a personal bank account is used for business activities. This unusual transaction pattern can trigger bank monitoring systems and lead to temporary freezes or compliance reviews.

A freeze gives you and the bank time to verify if the activity was truly authorized.

That is why unusual transaction freezes are precautionary freezes to stop hackers from illegally stealing your money.

Examples of unusual transactions include:

- Large purchases in distant locations you don’t usually shop or travel.

- Multiple failed or repeated attempts at odd transactions.

- Several small, rapid-fire payments.

- Strange recurring subscriptions you didn’t set up.

- Sudden high-value transfers to unfamiliar accounts.

- Foreign currency spending when you’re not abroad.

- High-volume business transactions mixed with low personal spending (Rare)

How to resolve an unusual transaction freeze

If you find yourself in an unusual transaction freeze, you should do the 2 following four steps to protect your accounts.

- If you use a PayPal account connected to your bank account, you must update travel schedules in your PayPal account to help avoid problems with locked accounts.

- Use two-factor authentication and monitor alerts so you can confirm (or deny) suspicious charges instantly with your banker via phone calls or your banking apps.

4.3. Debt-related freezes

Examples of debt-related freezes

Another common reason for a frozen account is unpaid debts. Creditors (like credit card companies, lenders, or even the government) can’t freeze your account directly. But with a court judgment, they can order your bank to do it. Once that happens, money can be taken from your account to cover:

- The debt you owe

- Court-approved fees

Examples of debts that can trigger a freeze include:

- Unpaid taxes to the tax authorities (IRAS, IRS, IRD)

- Student loans

- Car loans or personal loans

- Mortgages

- Divorce settlements

In these cases, both the creditor and your bank will notify you. You’ll usually get a court order first, then a notice from your bank once the freeze is in place.

Other scenarios for debt-related freezes

If you are a foreign worker working in another country with a working visa (Employment Pass in Singapore), you must do tax clearance (Pay all the taxes to IRAS) before leaving the country. IRAS and the company director can hold your Singapore bank accounts to pay off all your taxes.

In the US, the IRS can go further by imposing a tax levy — seizing your bank funds, property, and even garnishing wages until your tax debt is settled.

How to resolve debt-related freeezes

Our banking advisor recommends you take 4 practical actions to resolve debt-related freezes

- Set up automatic reminders or autopay for bills and loan installments.

- Create a monthly budget that prioritizes debt payments over non-essential spending.

- Keep all letters, emails, and agreements from creditors in one place.

- Call your bank or creditor as soon as you know you might miss a payment.

Our stress-free formula to pay off debts

If you are in the process of paying off debts, you can use our simple formula here to know how much debt you should pay off each month, and not be stressed about your cash flow: Income – Essential Expenses) ÷ 2 = Maximum debt payment.

For example, you earn 200,000 USD in net income per month from your company. Using our formula, you can have 10,000 USD to pay back debts per month with minimal mental strain

This way, you use half of your leftover money for debts and still keep the other half for savings, emergencies, or unexpected costs. It helps you pay down debt consistently without feeling broke or stressed.

4.4. Non-compliance freezes

Examples of non-compliance freezes

Every bank account comes with an agreement, and breaking those terms can get your account frozen.

This usually happens when customers:

- Provide inaccurate information (e.g., wrong address or false income details).

- Fail to submit required documents (like updated ID or proof of business activity).

- Don’t follow policies set out in the account agreement. (fall below standard account balance for more than 6 months,)

How to resolve non-compliance freeezes

These freezes are the easiest to resolve since the account holders just need to follow the requirements to lift the freeze.

- Keep your personal and business details updated (address, company ownership changes)

- Submit the requested documents on time

- Review your account agreement so you’re clear on what’s required.

4.5. Dormancy freezes

Examples of dormancy freezes

If your account sits unused for too long, it can raise red flags and trigger dormancy freezes. Because dormant accounts pose these 2 problems

- Dormant accounts are prime targets for fraudsters since they’re less likely to be monitored, and they use dormant accounts to split large sums of money into smaller chunks to make them harder to trace)

- Inactive accounts create maintenance costs for banks.

To reduce both risks, banks may freeze inactive accounts, and if inactivity continues, they may even close them.

For example, in the U.S., most states require banks to hand over dormant funds to the state’s unclaimed property office after 3–5 years of no activity. This process is called escheatment. Banks usually send notices before this happens.

How to resolve dormancy freezes

Based on our experience helping clients open accounts overseas in Singapore, Hong Kong, and the U.S, here are 3 simple actions you can take:

- Make small transactions regularly (deposit, transfer, or bill payment) every 2 weeks if there are no business activities

- Keep your contact details updated to avoid missing any inactivity alerts from the bank.

- Close or consolidate unused accounts instead of letting them sit idle and risk being frozen. (These dormant accounts also have you lose money due to the management account fee)

4.6. Businesses liquidation freezes

Important note

In a normal company closure (where the business is solvent), closing the bank account is actually the last step. That’s because the account is still needed to pay all outstanding debts to creditors and taxes to the government.

But if your company is insolvent (unable to pay debts), the bank account will be frozen as part of the liquidation process.

Businesses' liquidation freeze ensures no transactions interfere with the insolvency process and prevents new debts from piling up once liquidation begins.

Liquidation can happen in two ways:

- Voluntary liquidation initiated by the company’s directors or shareholders.

- A creditor’s petition where creditors formally demand repayment, and if ignored, the court can force the company into liquidation.

To proceed, creditors usually need to prove the company can’t pay its debts, and the outstanding debt must exceed a threshold set by local laws.

If you choose to close down your company, you must ensure you pay off all debts and taxes:

- Track your company’s solvency — know whether you can pay all debts before initiating closure.

- Settle taxes and creditor payments early to avoid forced liquidation.

- Plan your company closure properly so the account remains usable until final debts are cleared. (We recommend you seek support from professionals like Global Link Asia Consulting to help you close down your company)

4.7. Regulatory or legal investigation freezes

Examples of regulatory freezes

Sometimes, account freezes happen not because of your actions, but because of ongoing investigations.

Banks are legally obligated to cooperate with regulators, tax authorities, and law enforcement agencies. If your account is linked directly or indirectly to an investigation, it may be frozen until the matter is resolved.

This can happen in cases like:

- Ongoing tax audits or disputes.

- Investigations into money laundering or fraud.

- Regulatory compliance checks in highly regulated industries (e.g., finance, healthcare).

- Court orders related to lawsuits or judgments.

In August 2025, Singapore’s tax authority (IRAS) charged two men, aged 40 and 73, for their suspected involvement in a $181 million GST Missing Trader Fraud.

They allegedly set up four shell companies and created fictitious sales transactions between them at inflated prices. These sham sales were designed to fraudulently claim GST refunds from IRAS.

Companies unknowingly caught in the supply chain of such transactions have their bank accounts frozen to track the money flow.

How to resolve a regulatory or legal investigation freeze

From our experience working with international businesses, here are 3 simple but powerful actions you can take:

- Always run due diligence checks to ensure they’re legitimate and trustworthy.

- Maintain accurate invoices, contracts, and bank statements for at least 5 years to prove every transaction

- Get legal advice fast if your company is pulled into a regulatory inquiry; early action can save you from bigger risks.

5. The 2 solutions to avoid a completely frozen bank account

After helping clients open corporate bank accounts in Singapore, Hong Kong, the US, and 10+ other countries, one lesson our experts always recommend to our clients: it’s always easier to prevent problems than fix them later.

Here are 2 simple and powerful next steps you can do to protect your finances, your company's finances, and cashflow

- Keep your minimum balance so you don’t get hit with extra charges

- Even if you’re not using the account often, make small transactions now and then to keep it active.

- Check all your information changes and update them to your banks and the government

- Keep all your financial records the right way, and maintain them for at least 5 years.

If your KYC profile is suitable, we recommend opening two bank accounts:

- Open one account with a physical bank in your chosen country for services and stability.

- One additional account with a licensed digital bank as a backup for flexibility and smooth cash flow.

6. How can we help you avoid having your bank account frozen

You've known the 7 reasons and how to resolve each. Now it’s time to protect your business.

Take one action today. Just one.

- Maybe that’s setting up a reminder for your payment deadlines.

- Maybe it’s making a small transaction in your dormant account.

- Or maybe it’s calling your bank before a large transfer.

- Don’t wait until your account is frozen; prevention is always cheaper than a cure.

As a team with 10 years of experience helping hundreds of business owners open corporate bank accounts worldwide, we’ve seen how small steps can save companies from big disruptions.

Start today. Keep your accounts open, active, and stress-free.

If you need support to open a corporate bank account for your overseas company in Singapore, Hong Kong, the United States, the United Kingdom, Canada, and 10 other countries, we can help you

- Recommend the right bank and the right bank account for your needs

- Support you in opening a reliable, trusted digital bank account or traditional bank account

- Prepare necessary documents for account opening

- Schedule an appointment with a Singapore bank representative

- Monitor and assist in opening personal bank accounts (physical and digital)

7. FAQs about bank account freezing

Yes. Banks have the legal right to freeze your account without prior notice in specific situations. In the majority of cases, we support, if they notify you about the freeze, they will not give you any explanation for why it happens i

This is why maintaining clear records, compliant activity, and proactive communication with your bank is essential. Prevention is always easier than dealing with a sudden freeze.

The timeframe depends entirely on the cause of the freeze. If the issue is minor, such as account inactivity or a verification check, it can be resolved in a few days once you provide the required documents.

However, if the freeze is tied to debts, tax issues, legal disputes, or regulatory investigations, the process can stretch from 3 months to 2 years

The first step is to stay calm and gather information. Call your bank, your service provider right away to confirm why the account was frozen. Don’t rely on assumptions: a freeze due to suspicious activity is very different from one triggered by a creditor’s petition.

Next, secure your ongoing obligations. If you have automatic debits (e.g., rent, utilities, payroll), arrange alternative payment methods to avoid late fees or disruptions.

Third, document everything. Keep records of all communications with the bank, creditors, and authorities. This protects you if the situation escalates.

Finally, act decisively to resolve the root cause. Whether that means paying off a debt, submitting compliance documents, or hiring a lawyer, quick and professional action is key. A frozen account doesn’t fix itself, it requires you to take control of the process.

The impact is far more serious for businesses. A personal account freeze usually affects an individual’s access to funds, but a business account freeze can disrupt payroll, vendor payments, and cash flow. Banks also apply stricter scrutiny to corporate accounts.

A freeze might not just affect one account but could extend across all accounts linked to the company, its directors, or shareholders, especially in cases of suspected fraud, tax issues, or insolvency.

In most cases, deposits can still be made into a frozen account, but withdrawals, transfers, and outgoing payments are blocked. This means money can flow in, but you won’t be able to access it until the freeze is lifted.

Yes, the key is to act quickly and have a backup plan in place. Many businesses prepare by opening additional accounts in jurisdictions like Hong Kong or Singapore, so they can continue receiving payments and paying expenses even if one account is restricted.

This approach helps you:

- Deal with unexpected account freezes;

- Maintain cash flow without disruption;

- Keep your business running smoothly.

To increase your chances of success, it’s important to follow a structured, expert-guided approach when setting up and managing your bank accounts.

Read our guide here to increase your approval chances and avoid common mistakes.

With over a decade of experience serving as a trusted partner to more than 750 business owners seeking professional development and breakthroughs in the international market, we are an expert strategic corporate service provider helping you incorporate and operate successfully in 10 different countries

Our areas of expertise include:

- Strategic Consulting and Company formation in over 10 different countries worldwide such as Singapore, Hong Kong, the U.S., Australia, Thailand, Malaysia, and offshore destinations like BVI, Belize, Seychelles, and more.

- Account opening for personal and corporate bank accounts, as well as setting up PayPal and Stripe gateqays in countries like Singapore, Hong Kong, and the U.S..

- Tax Consulting and Preparation for SFRS IFRS financial reports, corporate income tax returns, VAT/GST (Value Added Tax/Goods and Services Tax), and more.

- Opreation support:

- Registered adress;

- Foreign consular legalization;

- Trademark and patent protection registration in Singapore and the US;

- Employment Pass application in Singapore and Hong Kong;

- Website design, international SIM number provision;

- DUNS registration.

With over 10 years of experience and a team of experts with 5 to 25 years of experience (international standard certifications) as well as direct partnerships with institutions such as OCBC, UOB, DBS, PayPal, and Stripe, we are proud to offer professional, legal, transparent, sustainable services with no hidden costs.

Global Link Asia Consulting Pte. Ltd. is pleased to announce the publication of the above insightful and informative article on our official website, Global Link Asia Consulting on 25th August 2025. The copyright for this article is exclusively held by Global Link Asia Consulting Pte. Ltd. Any unauthorized reproduction or distribution of this content without our express written permission is strictly prohibited. We value the protection of our intellectual property and appreciate your cooperation in adhering to these guidelines. Thank you for your continued support of Global Link Asia Consulting Pte. Ltd.