During 10 years of helping our clients expanding their business overseas in Singapore, Canada, the U.S and 10+ countries, many business owners ask us this question early on. “Can I just use my personal bank account for business?”

- It feels faster;

- It feels cheaper;

- And at the beginning, it feels harmless.

But it isn’t. You should not use personal bank account for your company and its related business transactions. Using a personal bank account for business is one of the most common, and costly mistakes founders make. And it shows up later, when the business is already running: 1 years if you are lucky, 5 years and the tax authority of another country send a letter asking you to clarify missing personal tax payment.

Our experts see this all the time. Startups, freelancers, even companies with real revenue still mixing personal and business funds. This isn’t just a “best practice” issue.

- It’s a compliance risk;

- It’s a tax risk;

- And in some cases, it’s a banking shutdown risk.

Why? Because banks, tax authorities, and payment providers don’t look at money the way founders do. They look at structure, traceability, and intent. And personal accounts fail on all three due to compliance, record-keeping, and tax complexities

In this guide, you’ll learn:

- What risks you’re actually taking when using personal bank account for business (even if “nothing has gone wrong yet”);

- How you should set up your business bank account the right way.

If you’re running a business, or planning to, this is something you need to get right early. Let’s get into this

1. The truth of using personal banks for business

It is true that there is not a regulation prohibiting the use of personal accounts for business transactions. However, the reality of day-to-day business is much more complex.

Let’s start with the basics.

1.1. What are business transactions?

Business transactions are financial activities directly related to running your company. They’re not personal spending. They’re not “owner convenience” payments.

They’re transactions made in the name of the business, for the purpose of generating or supporting revenue. In reality, some common business transactions you as a buisness owner encounter, are:

A simple rule to remember

If you are confused about business transactions. Ask yourself one question “ Would this expense exist if the business didn’t exist?”

If the answer is no, it is a business transaction. And it should belong in a business bank account. This clarity is exactly what banks, accountants, and tax authorities expect, and what protects you long-term.

| Category | What it covers | Examples |

| Software & Subscriptions. | Digital tools used for operations. | Accounting software (QuickBooks, Xero) , CRM systems, email marketing tools, cloud storage, project management tools. |

| Rent & Utilities. | Costs to operate your business location. | Office rent, coworking space fees, warehouse rent, electricity, water, internet, business phone plans. |

| Office Equipment & Supplies. | Tools and materials needed for daily work. | Laptops, monitors, printers, desks, chairs, stationery, POS machines. |

| Logistics & Operations. | Costs to deliver products or services. | Shipping fees, customs duties, fulfillment services, courier charges. |

| Legal & Professional Fees. | Compliance and advisory services. | Company incorporation fees, accounting services, tax filing, audit fees, legal consultations. |

| Employee Salaries & Contractors. | Payments to people working for your business. | Monthly salaries, freelance designers, developers, virtual assistants, commission payments. |

| Bank & Payment Fees. | Costs tied to receiving or sending money. | Payment gateway fees, bank transfer fees, merchant account charges. |

| Advertising & Marketing | Activities to promote your business | Google Ads, Facebook Ads, TikTok Ads, influencer payments, PR agencies |

1.2. What are the differences between a business account and a personal account?

Business account and personal account may look similar. They both hold money. They both send and receive payments. But they’re built for very different purposes.

You can see key differences highlighted in our table, prepared by our banking experts.

| Business account | Personal account |

A business bank account is designed to support company operations.

| A personal bank account is built for individual, day-to-day life.

|

2. Why you should not use your personal bank account for your company business activities

Using a personal bank account for business rarely causes problems at first. It’s convenient and easy to access, especially since most founders already have a personal account. That’s why many founders continue using it in the early stages of business.

It works. Until it doesn’t. And problems show up later:

- When banks review unusual transaction patterns;

- When payment providers run compliance checks;

- When accountants can’t clearly separate personal and business transactions;

- The most serious issue arises when tax authorities question the source of the income and the applicable tax rate—whether it should be classified as business income or personal income, and which tax rate applies during an account audit.

At that point, fixing it is slower, more expensive, and far more stressful. In fact, there are 6 problems that our banking experts, tax specialists, and business consultants point out you may face if you use a personal bank account for your company without considering the long-term consequences.

Banks today follow strict anti-money laundering (AML) regulations.

If a personal account suddenly receives frequent payments from different sources, the activity look similar to fraud or money-laundering transaction layers. As a result, banks may freeze the account, request explanations, or even close it until the purpose of the transactions is verified.

A common example is YouTubers or online creators receiving platform payouts into their personal accounts. Even though the income is legitimate, the bank may still flag it as commercial activity in a personal account, which creates hidden risks.

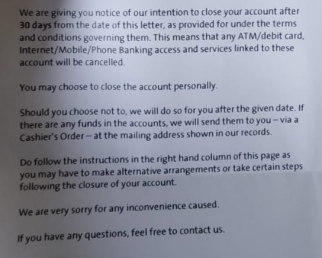

Account shutdown notice from OCBC (Rare case)

Account shutdown notice from OCBC (Rare case)

Another factor is future regulation. Governments are gradually tightening control over financial transactions and tax reporting. Business income flowing through personal accounts may face stricter monitoring over time.

For long-term stability, separating business banking and personal banking is usually the safer approach.

Managing business finances through a personal bank account complicates bookkeeping and accounting.

Mixing personal and business transactions makes it difficult to accurately track income, expenses, and profits. This increases the likelihood of errors in financial statements and tax filings, which can lead to penalties or compliance issues.

A dedicated business bank account keeps records clean, makes collaboration with accountants easier, and allows faster verification by tax authorities. Many business accounts also integrate directly with accounting software, improving efficiency.

Business expenses are typically tax-deductible, but only when they can be clearly identified and properly documented. Using a personal account blurs the line between personal and business expenses, making it harder to substantiate deductions. This can result in overpaying taxes or submitting inaccurate tax returns.

A separate business account provides a clear audit trail and supports accurate, defensible tax reporting.

Separating personal and business finances is essential for effective cash flow management.

When transactions are mixed, it becomes difficult to assess true business performance, forecast expenses, or plan for growth. Poor visibility into cash flow increases the risk of overspending or unintentionally using business funds for personal needs.

A business bank account enables clear tracking of inflows and outflows, helping business owners make informed financial decisions with confidence.

Receiving payments through a personal bank account can negatively impact how clients perceive your business. Many clients view payments to personal accounts as unprofessional or informal.

Some corporate clients and enterprises require payments to be made to an account that matches the registered business name. Using a business bank account enhances credibility, improves client confidence, and can increase opportunities with larger partners.

Additionally, investors and lenders assess a business’s financial health by reviewing its financial records. Using a personal account for business transactions can raise concerns about transparency, organization, and professionalism.

A dedicated business bank account supports clean financial records and helps establish business credit history. Business accounts also provide access to financing options such as business loans, credit cards, and credit lines that are not available through personal accounts.

Certain business structures, such as limited liability companies and corporations, are designed to protect personal assets from business liabilities. This protection depends on a clear legal and financial separation between the owner and the business.

When personal and business funds are mixed in the same account, that separation is weakened. In legal disputes, courts may conclude that the business is not truly independent, potentially allowing creditors to pursue personal assets through a process known as piercing the corporate veil.

Using a personal bank account for business also increases the risk of account freeze, account suspension or closure.

Personal accounts are intended for low-volume, non-commercial transactions. As a business grows, higher transaction volumes and larger payment amounts may exceed personal account limits or violate bank terms. This can trigger compliance reviews, temporary freezes, or permanent account closures, disrupting business operations and cash flow.

3. Are there any exceptions to using a personal bank account for business?

In general, we strongly advise having two separate bank accounts:

- One business account, used strictly for company income and expenses.

- One personal account used only for your personal spending and savings.

Keeping them separate protects your company, keeps accounting clean, and makes tax reporting much easier. It also builds credibility with banks, investors, and regulators.

So when does a personal bank account make sense? From our banking expert advice, there is 3 important scenarios:

- When you need to invest (An investment account), or save money (A saving account);

- When you are a freelancer / a self-employed person (Sole proprietor);

- When you distribute profit from your company.

3.1. When you need to invest or save your money

If you plan to:

- Build long-term wealth;

- Invest in stocks, funds, or other assets;

- Set aside emergency savings;

- Manage personal financial goals.

A personal investment or savings account becomes the right structure.

From there, you can invest your hard-earned money into assets such as stocks, funds, or other long-term investments to build personal wealth over time. Later, if your personal investments generate profits, you may decide to reinvest that personal capital back into your company as new capital or a shareholder loan if needed.

In other words:

- Business money stays in the business.

- Personal wealth grows through personal investment accounts.

This separation helps you build wealth while maintaining proper financial structure for your company.

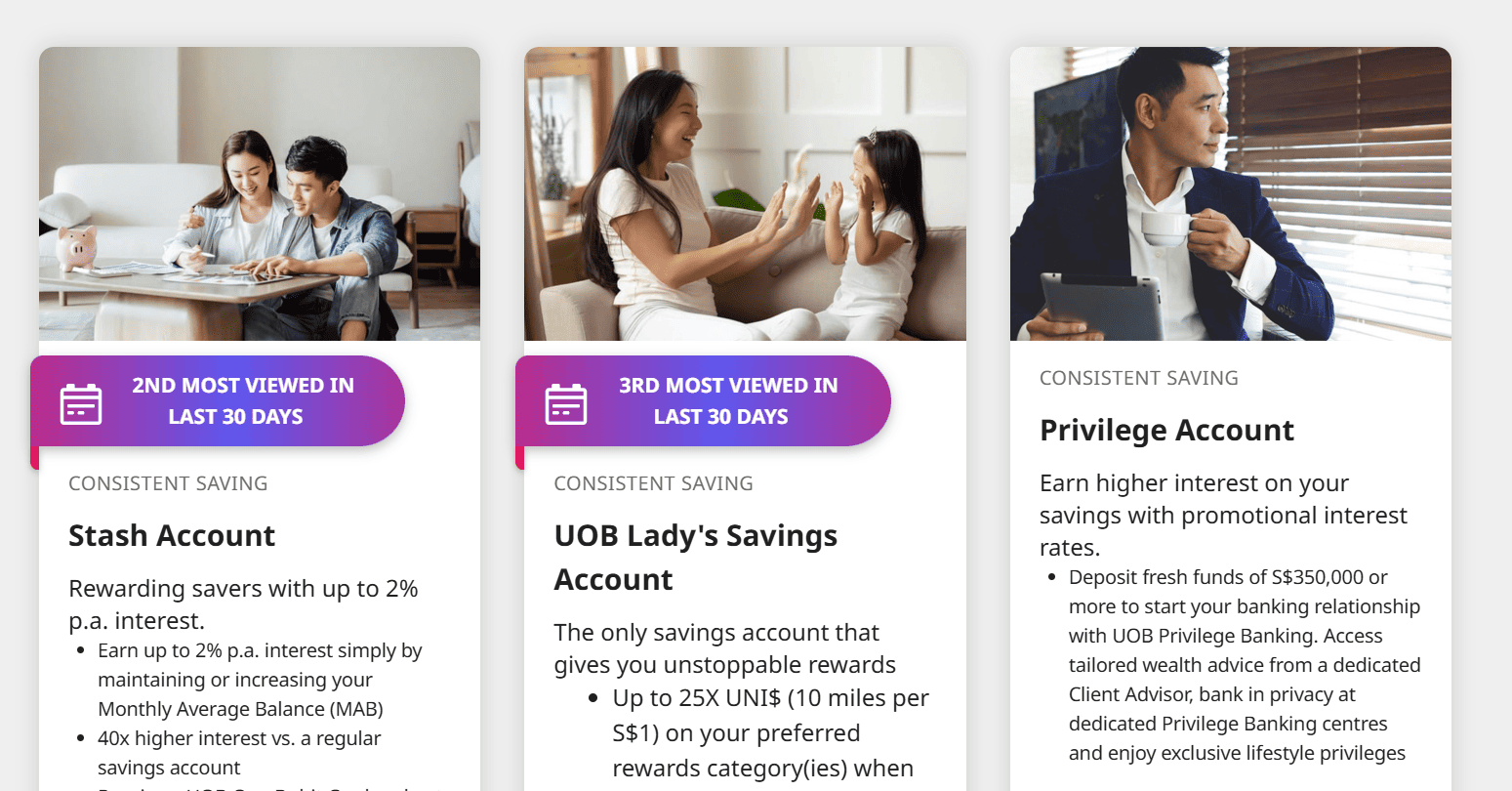

Saving accounts from UOB

3.2. When you are a freelancer / a self-employed person (Sole proprietor)

If you operate as a freelancer, consultant, or self-employed professional, your legal structure is different from a registered company.

In this case, you are considered unincorporated.

This means you and your business are legally the same entity.

As a result:

- The income you earn belongs directly to you;

- There is no legal separation between business and personal assets;

- You are 100% personally liable for your business activities.

Because of this structure, it is acceptable to use a personal bank account as your “business” account.

In practice, this means:

Clients can pay directly into your personal bank account

Business income and expenses can be processed through the same account

Your earnings are treated as personal income, rather than company revenue

However, many freelancers still choose to dedicate one personal account specifically for business transactions. This helps you:

- Track income from clients more clearly;

- Separate business expenses from daily spending;

- Prepare tax reporting more easily;

- Maintain better financial discipline.

So while a sole proprietor can use a personal bank account for business purposes, having a structured banking setup still makes managing your finances much easier.

3.3. When you distribute profit from your company.

If your company has made a profit, you are entitled to receive that profit as:

- Dividends (profit distribution to shareholders), or;

- Director remuneration/ salary (depending on your structure), or;

- Returns from shares or investments.

In this case, the approach should be:

- The company declares profit;

- The company transfers the approved amount from the business bank account to your personal bank account, clearly recorded as dividend or shareholder remuneration.

When you transfer profit properly:

- Your business account remains clean and transparent;

- Your financial statements stay accurate;

- Tax treatment is clearer;

- You protect limited liability;

- You avoid compliance and audit risks.

And if you set up your personal bank account the right way (Our banking expert can consult and support you with that), your finance blossoms even more.

4. Your roadmap to business bank account adoption

You don’t always need a business account on day one. But there are clear moments when opening one stops being optional and starts being essential. You can think of it as a simple three-phase journey.

Ready to level up? Open a corporate bank account in Singapore

Singapore offers one of the world’s most reliable banking systems, multi-currency capabilities, strong regulatory credibility, and seamless integration with global payment and accounting tools

If you’re ready to use banking as a financial tool to operate more efficiently, scale internationally, and build long-term credibility, a Singapore corporate bank account helps take your company operations to the next level.

You should pause and consult a professional if:

- You’re moving beyond casual or one-off transactions

- You’re unsure whether your business structure requires financial separation

- You plan to operate across borders or in multiple currencies

- You want to avoid future tax, compliance, or banking issues

At this stage, the goal is clarity. Understanding your legal structure, banking obligations, and growth plans helps you avoid costly corrections later.

Outcome: You know whether a business account is recommended or mandatory for your setup.

Our experts can help you make clear of your situation and a suitabe solutions: Account with digital banks, or traditional banks

This is the execution stage. A business account becomes necessary once your business reaches operational or regulatory thresholds.

You should open a business bank account if:

- Your business is registered as an LLC, corporation, partnership, or equivalent

- You operate under a registered business name or DBA

- Clients or platforms require payments to a business-named account

- Your bank prohibits business use of personal accounts

- You need clean financial records for tax filing or audits

Opening a business account at this stage protects compliance, improves credibility, and enables proper financial management.

Outcome: Your business finances are formally separated, compliant, and ready to scale.

With our support, you can open your account with a 98% success rate, guided by a proven KYC checklist and 10+ years of banking expertise: We help you choose the right bank and account type to support your business not just today, but for the next five years.

This is the optimization stage. Once your business account is active, new capabilities become available.

With a business account, you can:

- Track cash flow accurately and plan growth

- Access multi-currency payments and international banking tools

- Integrate accounting software for faster reporting

- Build business credit history

- Qualify for financing, loans, or merchant services

- Preserve value and earn stable returns by holding company funds in strong currencies. such as USD, EUR, SGD, CAD, AUD, GBP, and others.

This phase is about leverage. A business account is no longer just a requirement—it becomes an operational advantage.

Outcome: Your business gains financial visibility, credibility, and access to growth opportunities.

You can store company funds in savings accounts denominated in strong, stable currencies such as USD, EUR, SGD, CAD, AUD, GBP, and others. This helps preserve value and generate steady returns each year on surplus company funds that are not being used for operations.

In practice, our clients have achieved returns of up to 10% per year on their company funds by managing risk effectively and holding assets in USD instead of volatile local currencies.

5. Open your business bank account today

When business income runs through a personal account, the risks don’t show up immediately. At first, it feels convenient. Later, it becomes expensive.

Effective business banking looks different.

It’s built on:

- Clear separation between personal and business finances;

- Clean records that stand up to tax reviews and audits;

- Banking structures that support growth, not restrict it.

When those pieces are in place, banking stops being a risk—and starts supporting operations. If you want to know when a business account becomes essential, explore our Business Banking Adoption Roadmap above.

For founders who want a more sustainable financial structure, we often recommend setting up both a personal bank account and a business bank account at the same time. This allows you to:

- Receive and manage business income through a dedicated corporate account;

- Transfer profits properly to your personal account;

- Separate operational funds from personal wealth;

- Build a banking structure that works effectively as your business grows.

Our experts help founders open accounts with a 98% success rate, using proven KYC frameworks and 10+ years of banking experience.

- Recommend the right bank and the right bank account for your needs;

- Support you in opening a reliable, trusted digital bank account or traditional bank account;

- Prepare necessary documents for account opening;

- Schedule an appointment with a Singapore bank representative;

- Monitor and assist in opening corporate bank accounts (physical and digital).

6. FAQs about using personal bank account for company activities

Short answer: No. A new bank account does not count as a business account just because you don’t spend the earnings.

A bank account is considered a business account based on how it’s designated and used, not whether you withdraw or spend the money.

What actually matters:

- Whose name is on the account (business vs. individual);

- The account type approved by the bank (personal vs. business);

- The purpose of transactions (commercial activity vs. personal use).

If business income flows into a personal account:

- It’s still treated as business activity;

- Banks may flag or freeze the account;

- Tax authorities may question income classification;

- Legal separation between you and the business is weakened.

Even if the money just “sits there.” To be compliant and protected, business income should go into a business account.

A personal bank account is appropriate after business income has been properly earned, recorded, and distributed.

For example, if you receive salary, dividends, or profit distributions from your company and plan to use the funds for personal expenses, or transfer them to your personal account in your home country, using a personal bank account is the correct approach.

This separation ensures that business and personal finances remain clearly distinct, avoids unnecessary entanglement between accounts, and supports accurate accounting, tax reporting, and compliance.

Best practice: Yes, you should. Having a separate business bank account makes bookkeeping much easier and helps you clearly separate money used for personal and business activities. This reduces errors, saves time during tax filing, and gives you better visibility into your cash flow.

In reality: It’s not always mandatory. As a sole proprietor, you and your business are legally the same entity. You do not need to open a separate account for your business

However, as income grows, transactions increase, or you start working with clients and platforms that expect a business-named account, opening one becomes highly advisable to avoid confusion, compliance risks, and operational friction.

Bank transfers can sometimes take longer than expected due to several factors. These include batching or ACH processing times, the involvement of intermediary banks (especially for international transfers), and delays from external banks.

Additionally, transfers may be held for fraud detection checks (such as Anti-Money Laundering and Counter-Terrorism Financing regulations), or simply delayed bank holidays when financial institutions are closed.

If you want to learn more about each reason, and discover practical tips to speed up your transfers, check out our comprehensive guide: Why do bank transfers take so long? (+ How to speed them up).

With over a decade of experience serving as a trusted partner to more than 750 business owners seeking professional development and breakthroughs in the international market, we are an expert strategic corporate service provider helping you incorporate and operate successfully in 10 different countries

Our areas of expertise include:

- Strategic Consulting and Company formation in over 10 different countries worldwide such as Singapore, Hong Kong, the U.S., Australia, Thailand, Malaysia, and offshore destinations like BVI, Belize, Seychelles, and more.

- Account opening for personal and corporate bank accounts, as well as setting up PayPal and Stripe gateqays in countries like Singapore, Hong Kong, and the U.S..

- Tax Consulting and Preparation for SFRS IFRS financial reports, corporate income tax returns, VAT/GST (Value Added Tax/Goods and Services Tax), and more.

- Opreation support:

- Registered adress;

- Foreign consular legalization;

- Trademark and patent protection registration in Singapore and the US;

- Employment Pass application in Singapore and Hong Kong;

- Website design, international SIM number provision;

- DUNS registration.

With over 10 years of experience and a team of experts with 5 to 25 years of experience (international standard certifications) as well as direct partnerships with institutions such as OCBC, UOB, DBS, PayPal, and Stripe, we are proud to offer professional, legal, transparent, sustainable services with no hidden costs.

Global Link Asia Consulting Pte. Ltd. is pleased to announce the publication of the above insightful and informative article on our official website, Global Link Asia Consulting on 18th December 2025. The copyright for this article is exclusively held by Global Link Asia Consulting Pte. Ltd. Any unauthorized reproduction or distribution of this content without our express written permission is strictly prohibited. We value the protection of our intellectual property and appreciate your cooperation in adhering to these guidelines. Thank you for your continued support of Global Link Asia Consulting Pte. Ltd.