Business is changing fast.

- Cross-border payments are normal;

- Remote partners, clients and your employees are everywhere;

- And founders are managing revenue in 3–5 currencies at once.

But one thing hasn’t changed: If you structure your banking properly, you gain control, flexibility, and financial clarity. Not by opening random accounts. But by choosing the right types, for the right purpose.

Numerous options from banks

The right business bank accounts help you:

Separate operating cash from savings

Manage international payments efficiently

- Reduce FX losses;

- Accept global customer payments;

- Protect funds for tax and compliance;

- Build credibility with partners and investors.

Whether you're a startup, SME, e-commerce seller, or international group, these 7 account types form the foundation of smart financial management. Let’s break them down.

| Account type | Purpose |

| Business checking | Everyday account for handling daily transactions, payroll, bills, and operational expenses |

| Business savings | Interest-earning account for setting aside surplus cash or emergency funds |

| Business money market account (MMA) | Hybrid checking-savings account offering higher interest with limited transaction flexibility |

| Business certificate of deposit (CD) | Fixed-term deposit account with higher guaranteed interest in exchange for locking funds |

| Merchant account | Payment processing account that enables businesses to accept credit cards and electronic payments |

| Multi-currency account | Centralized account for holding and managing multiple currencies to support international operations |

1. First, do you need to open all the accounts in this article?

No, you do not need to open all types of bank accounts for your busisness. Most businesses can operate perfectly well with just three core accounts.

We have not seen too many founders waste time opening 6 different business accounts in their first month because some blog post told them they "needed" everything. That's overkill, especially when you're just getting started.

Here's what you actually need right now:

- Business checking account: This handles your daily operations. Customer payments come in, vendor invoices go out, payroll gets processed. Every business needs this from day one;

- Business saving account: This is where you park your emergency fund (3-6 months of operating expenses) and any surplus cash you won't touch for 30+ days to a year. It earns interest while staying liquid;

- Multi-Currency Account (only if you operate internationally): If you're invoicing foreign clients, paying overseas suppliers, or running operations across borders, this saves you thousands in exchange rate markups and wire fees. If you're purely domestic? Skip it.

That's it. Three accounts. You can run a $1M+ business on this foundation alone.

As your business scales, financial optimization becomes a competitive advantage. What costs you $500 at $100K in revenue costs you $50,000 at $10M in revenue. Small inefficiencies compound. This is when you start diversifying your banking strategy:

- Money Market Account;

- Certificate of Deposit (CD);

- Merchant Account.

At the enterprise level, every basis point matters. A company processing $10M annually in foreign transactions might save $100K per year just by optimizing their multi-currency strategy.

These details seem minor when you're doing $100K in revenue. They become material when you're doing $1 M and more.

2. Business checking account (Business current account)

Best for everyday use and unexpected business spendings.

Example of a business current account from CMIB

A business checking account has been the backbone of company finances for decades. Daily deposits, bill payments, payroll processing, vendor transfers, it handles almost everything you need to run your financial operations at scale.

What makes it different from a personal account (link bài personal account for business) isn't just the name on the card. You get higher transaction limits, advanced payment integrations, and tools built specifically for business workflows.

Depending on bank policy, business checking accounts may pay interest (or pay very little compared to savings accounts, and have other useful purposes (Multi-purpose account). But that's not the point. This account exists for velocity, not growth.

Example of a business integrated account (Multi-purpose account) from HSBC

2.1. Handle every transaction type in one place

A business checking account is your go-to for managing cash flow. It connects to every payment method your business touches throughout the day.

You can deposit funds through multiple channels:

- Electronic transfers and ACH payments;

- Mobile check deposits (snap a photo, done);

- Wire transfers for larger amounts;

- Branch or ATM deposits when you need them.

And moving money out is just as flexible. Write checks, send wires, swipe your debit card, or schedule automated payments through online banking. Most accounts also integrate directly with QuickBooks, Xero, or whatever accounting software you're already using.

Let's say you're running an e-commerce business, selling handmade products from South East Asia to the U.S market. You might receive customer payments via Stripe, pay your supplier through ACH, cover ads with your debit card, and send payroll via direct deposit, all from the same checking account.

2.2. Watch your transaction

Here's something that catches newer business owners off guard: many checking accounts cap your monthly transactions or have a ‘fall-below-deposit' policy. Go over that limit, and you'll see fees start piling up.

For example, a standard account might include 200 transactions per month. After that, you might pay $0.50 per transaction. If you're processing 300 transactions monthly, that's an extra $50 in fees you weren't planning for.

Another example is the required deposit for each month is 5000 SGD, but you only have 4000 SGD in your account. In this case, you have to pay "fall-below' fee to the bank

The workaround? Some online-first business banks offer unlimited transactions but restrict cash deposits since they don't have physical branches. Know your business model before you choose.

3. When do you actually need a business current account?

Every business should open a checking account the moment they open a company/business: Startup, LLC, corporations, private limitedd, partnership, etc.

If you're operating as a business entity, you need business banking.

| Pros | Cons |

| Essential for daily business operations | Checking accounts don't pay interest |

| Multiple deposit and payment methods in one place | Transaction limits can trigger unexpected fees |

| Integrate with accounting software and business tools | May require minimum balances to avoid monthly fees |

| Separate personal and business finances legally | Setup requires business documentation (EIN/TIN, formation papers) |

| Build financial credibility with vendors and partners | Online-only accounts or digital bank account) may limit cash handling options |

4. Business saving accounts

Best for setting aside surplus cash and building an emergency fund.

A business savings account has been the default parking spot for excess capital for decades. Emergency reserves, tax payments, seasonal cash cushions; it gives your money a safe place to sit while earning at least some return.

The interest rates aren't exciting. Most business savings accounts pay somewhere between 0.01% and 5% APY (Annual Percentage Yield) depending on the bank. But that's still better than letting $50,000 sit in checking earning nothing.

What you gain in interest, you lose in flexibility. Savings accounts restrict how often you can move money around — federally capped at six withdrawals per month in the US. Most don't let you write checks. And excessive cash deposits might trigger limits or fees depending on your bank.

But if you're holding capital you won't need for 30+ days, a savings account beats checking every time.

Example of a business saving account from Bank of China

5. Earn interest while you sleep

A business savings account is my go-to for money that needs to stay liquid but doesn't need to move daily.

Let's say you run a landscaping business. You make 70% of your annual revenue between April and September. By July, you've built up $80,000 in cash, but you know you'll need it to cover payroll and expenses through the winter.

If you leave that $80,000 in checking at 0% APY, you earn nothing. Move it to a high-yield business savings account at 4.5% APY, and you'll earn roughly $1,800 over six months — just for parking it somewhere smarter.

Most accounts also let you create sub-accounts for specific goals. You might have one for your emergency fund, another for quarterly tax payments, and a third for equipment upgrades. Same account, organized by purpose.

Tip from our banking experts

If you’re holding cash to pay overseas partners or creditors, and you’re worried about inflation or currency depreciation: Consider switching into a stronger currency (HKD, SGD, USD, EUR, GBP, etc) and keeping it in a high-yield savings account.

- You protect your capital from losing value;

- You earn interest on idle funds;

- And that extra return can be reinvested back into your business

- A win-win situation.

5.1. When should you open a saving account?

Our banking experts recommend opening a business savings account when you hit any of these scenarios:

- You have seasonal cash flow swings: Retail businesses that spike during Q4, tax firms that earn heavily in Q1-Q2, or construction companies with summer peaks — if your revenue isn't steady year-round, you need somewhere to store the surplus months to fund the lean ones.

- You're building an emergency fund: We suggest 1-2 years of operating expenses in reserves. A savings account keeps that cushion separate from daily operations while still earning interest.

- You're setting aside money for known future expenses: Quarterly estimated taxes, annual insurance premiums, equipment replacement funds — if you know cash will go out in 60-120 days, park it in savings until then.

- You want higher returns without market risk: Unlike investing excess cash in stocks or bonds, savings accounts are FDIC-insured up to $250,000. You won't lose principal, even if the market crashes.

| Pros | Cons |

| Earns interest on idle cash (unlike checking) | Interest rates still relatively low compared to other investments |

| Goverment-insured up per depositor (For example: FDIC-insured up to $250,000 per depositor) | Interest earned is taxable as ordinary income (Depending on the country poplicy) |

| Safe place to build emergency reserves or seasonal cushions | May require minimum balances to avoid monthly fees |

| Can be linked to checking for easy transfers | Not suitable for frequent transactions (althrough some banks have flexible policy to help you withdraw money direcly from your saving account, you lose interest the moment you do it) |

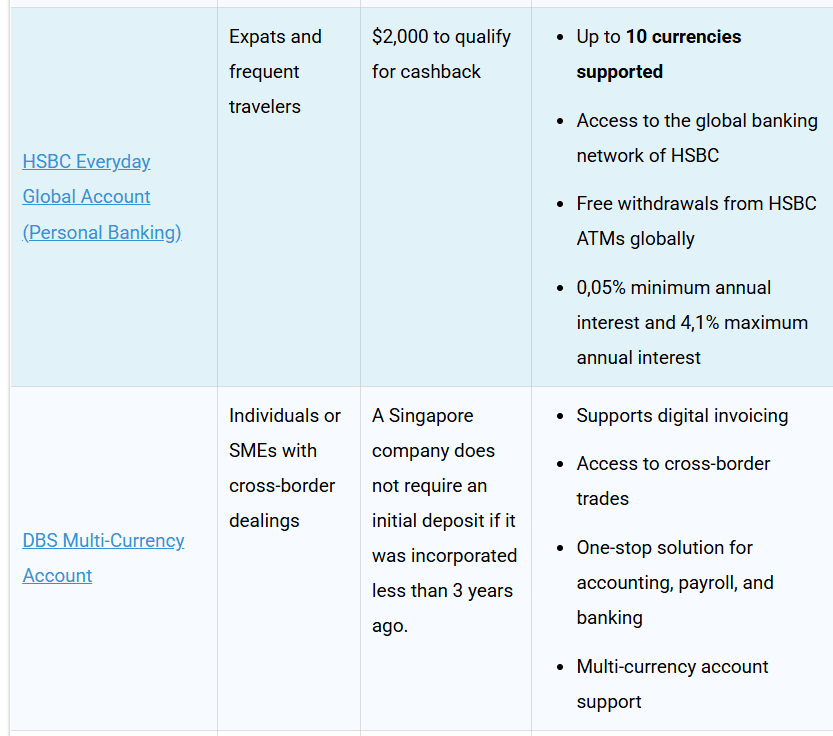

6. Multi currency account

Best if you need to pay overseas suppliers and receive customer funds in different currencies

Examples of multi currency account from our in-depth article

A multi-currency account help you hold Euros, British pounds, Japanese yen, Chinese yuan and US dollars in one place, no need to open separate foreign bank accounts in each country you operate in.

Top 5 multi currency account in Singapore you must know

If you’re doing business across borders, a normal bank account won’t cut it.

Exchange fees, slow transfers, hidden conversion spreads — they quietly eat into your margins.

That’s why choosing the right multi-currency account in Singapore matters more than most founders realize.

We’ve broken down the top 5 multi-currency accounts in Singapore, read our expert-written article here.

6.1. Unlock global payment the right way without extra fee

What makes these accounts powerful isn't just convenience. It's control. You can receive payment from a UK client in pounds, hold those pounds until the exchange rate improves, then convert to dollars when it makes financial sense.

With a traditional business checking account, you'd be forced to convert immediately at whatever rate your bank offers — which is typically 3% - 5% worse than mid-market rates.

Let's say you run an e-commerce business selling to customers across Europe, the UK, and Australia. Instead of converting every euro payment to dollars the moment it arrives (and losing 4% to exchange fees each time), you hold euros in your multi-currency account and only convert when you actually need dollars — or better yet, use those euros directly to pay European suppliers.

On $500,000 in annual foreign revenue, avoiding unnecessary conversions can save you $15,000 - $20,000 per year in hidden exchange rate markups alone.

6.2. When a multi-currency account is essential?

You need a multi-currency account if any of these scenarios apply:

If you're billing customers in their local currency (EUR, GBP, CAD, etc.) more than a few times per month, forced conversions at bad rates are silently draining thousands from your revenue.

Paying a European supplier in euros from a EUR balance costs you 0.5% - 1% in fees. Paying them in euros from a USD checking account costs 3% - 5% plus international wire fees ($35 - $50) and intermediary bank fee. The math is obvious.

If you have offices, employees, or operations in different countries, you need to manage payroll, rent, and expenses in local currencies without constant conversion drag.

Holding balances in multiple currencies gives you natural diversification. If the USD weakens 5% against the EUR, your euro balance just became 5% more valuable in dollar terms.

7. Business money market account

Best if you want the benefits of both a savings and checking account , and can meet the higher balance requirement.

A business money market account has been the middle ground between savings and checking for years.

Higher interest rates than savings, more access than a typical high-yield account — it's built for businesses that want their cash to work harder without completely locking it away.

Example of a money market account form Armed Forces Bank

7.1. Earn more without sacrificing liquidity

MMAs typically pay 0.5% - 1.5% more than standard business savings accounts. And most use tiered rate structures, meaning the more you deposit, the higher your APY climbs. For example, Park $100,000 instead of $10,000, and you might jump from 3.5% to 5.0% APY — an extra $1,500 per year just for having more on deposit.

What makes MMAs different from savings isn't just the rate. It's the access. You get check-writing privileges and debit card transactions, similar to a checking account. But you're still capped at six withdrawals per month under federal rules, so it's not meant for daily operations.

The tradeoff? Higher minimum balances. While a business savings account might require $100 to open, MMAs often start at $2,500 - $10,000. Some banks won't even open one unless you're depositing $25,000+.

7.2. Don’t confuse this with money market funds

Here's a critical distinction: a Money Market Account (MMA) is not the same as a Money Market Fund.

If someone pitches you a "money market" product, clarify which type they mean. The names sound identical, but the risk profiles are completely different.

| Money Market Account (MMA) | Money Market Fund |

|

|

8. When do you really need a MMA account?

Our banking experts recommend a business money market account when you fit these criteria:

- Your savings account rate feels too low: If you're earning 2.5% in savings but see MMAs offering 4.5% - 5.0%, and you have at least $10,000+ to move, the upgrade pays for itself immediately.

- You have a large cash reserve you might need to tap: Emergency funds, project budgets, acquisition war chests — if the balance is high enough to hit upper-tier rates and you want check-writing access just in case, MMAs are ideal.

- You want better returns without market exposure: Unlike stocks, bonds, or money market funds, MMAs are FDIC-insured. You get higher yields than savings with zero principal risk.

- You can meet the minimum balance requirements comfortably: If maintaining $10,000 - $25,000 minimum strains your cash flow, stick with a regular savings account. Dipping below the minimum often triggers monthly fees that eat your interest earnings.

| Pros | Cons |

| Often higher interest rates than standard savings | Higher minimum balance requirements ($2,500 - $25,000 and more) |

| Tiered rates reward larger deposits with better APY | Falling below minimum balance triggers monthly fees |

| Check-writing and debit card access for flexibility | Not suitable for frequent transactions or daily operations |

| Combine liquidity of checking with earnings of savings | Rates can change — not locked in like CDs |

| Good for large reserves that need occasional access | Some banks reserve MMAs for high-balance customers only |

9. Business certificates of deposit

Best for parking surplus cash you won’t need for a set period of time.

A business CD has been the go-to account for guaranteed returns for decades. Higher rates than savings or money market accounts, zero market risk, fixed returns you can plan around — it's built for cash you absolutely won't touch for months or years.

Example of a money market account form Bank of America

The tradeoff is access. Once you deposit funds into a CD, they're locked until the maturity date. Try to pull money out early, and you'll face penalties that can wipe out months of interest earnings. Some banks charge three months' interest for early withdrawal on a 6-month CD, or up to a year's worth of interest on a 5-year term.

But if you know you won't need the cash? CDs consistently pay 1% - 2% more than high-yield savings accounts. On a $100,000 deposit, that's an extra $1,000 - $2,000 per year just for committing to a timeline.

The interest rate stays fixed for the entire term, which cuts both ways. If rates drop after you open your CD, you're protected. If rates spike, you're stuck earning less than new depositors.

9.1. The early withdrawal penalty you need to understand

Here's what catches business owners: CD penalties aren't just fees. They eat directly into your interest earnings — and sometimes your principal.

Here is an example our expert want to use to illustrate our point:

A typical penalty structure looks like this:

- 3-month CD: forfeit 90 days of interest

- 6-month CD: forfeit 180 days of interest

- 12-month CD: forfeit 6 months of interest

- 5-year CD: forfeit 12 months of interest

So if you open a 12-month CD earning 5% APY on $50,000, you'd earn $2,500 at maturity. But withdraw after just 6 months, and you'll forfeit half that interest ($1,250) as a penalty. Your actual return drops to 2.5% APY — lower than if you'd just used a savings account.

Even worse: if you withdraw very early (say, 2 months into a 12-month CD), you might not have earned enough interest yet to cover the 6-month penalty. In that case, the bank takes the penalty from your principal. You get back less than you deposited.

Bottom line: only open a CD if you're absolutely certain you won't need the money before maturity.

The CD laddering technique

Let's say you have $40,000 in reserves. Instead of one $40,000 CD for 2 years, you open 2 separate CDs for 1 year each

- $20,000 in a 1-year CD at 4.75% APY;

- $20,000 in a 2-year CD at 4.50% APY.

After one year, your first CD matures. You now have three options:

- Take the cash if you need it;

- Reinvest into a new year CD at whatever rate is available;

- Keep it liquid in savings/MMA.

A year later, your second CD matures. Same options. Now you have $20,000 maturing every single year, giving you regular decision points without locking everything away indefinitely.

The benefit? You're earning higher long-term rates on most of your money, but you're never more than 12 months away from accessing a chunk of it penalty-free. It's the best of both worlds.

9.2. When do a certicate of deposit make sense in your case?

I recommend business CDs when you hit these specific scenarios:

- You have a known future expense with a fixed date: If you're saving for a $75,000 equipment purchase in 18 months, a CD maturing right before that date guarantees your rate and keeps you from touching the funds early;

- Current rates are attractive and you expect them to drop: If CDs are paying 5% today but economists predict rate cuts over the next year, locking in that 5% for 12-24 months protects you from declining returns.

- You've maxed out your MMA tiers and still have excess cash: Once you hit the top tier in your money market account, additional deposits earn the same rate. Moving the surplus into CDs can often boost your blended return by another 0.5% - 1.0%.

- You struggle with the temptation to spend reserves: The lockup period forces discipline. If you know you'd be tempted to dip into an MMA for non-emergencies, a CD removes that option entirely.

| Pros | Cons |

| Often higher interest rates than standard savings/MMA | Funds completely locked until maturity |

| Fixed rate protects you if market rates drop | Early withdrawal penalties can eliminate months of interest |

| Predictable returns make financial planning easier | Not suitable for emergency funds or unpredictable cash needs |

| CD laddering provides regular access while earning higher rates | Rates can change — not locked in like CDs |

| Good for large reserves that need occasional access | Automatic rollover can lock you into worse rates if you forget |

10. Merchan bank account

Best for business that need to accept credit cards and electronic payments from customers

A merchant account has been the backbone of electronic payments for decades. Credit cards, debit cards, Apple Pay, Google Pay: None of it works without this specialized account sitting between your customers and your business bank account.

Your regular business checking account can't process card payments directly. It lacks the infrastructure, security protocols, and payment network connections required to handle electronic transactions. That's where merchant accounts come in.

Example of a money marrket account form M&T Bank

Let's say you run an e-commerce store selling outdoor gear. A customer in California orders a $500 tent using their Visa card. Here's what happens behind the scenes:

Here's how it actually works:

- A customer pays you $500 with a credit card. That money doesn't hit your checking account immediately. It may go through payment gateway like Stripe, Paypal, Authorize to capture the card details.

- It lands in your merchant account first, where it sits for 1-3 business days (longer or shorter )while the payment processor verifies the transaction, checks for fraud, and settles funds with the card networks.

- Then it transfers to your checking accounts, minus processing fees that typically range from 1.5% to 3.5% per transaction.

On that $500 sale, you might pay $12.50 in fees (at 2.5%). Do 200 transactions per month, and you're spending $2,500+ annually just to accept cards. But for most businesses, that's still cheaper than turning away the 80%+ of customers who prefer to pay online in the age of AI and digital transformation.

Compare at least 3 providers on total cost, not just headline rates

10.1. When a merchant account is non negitiable?

You need a merchant account if any of these apply:

- You sell online or via mobile app: E-commerce businesses can't survive on cash and checks. If you're selling through Shopify, WooCommerce, or a custom site, you need merchant services to process cards.

- You accept in-person card payments: Retail stores, restaurants, salons, gyms — if customers expect to swipe, tap, or insert their card, you need the infrastructure to handle it.

- You run a subscription or recurring billing model: SaaS companies, membership sites, subscription boxes — merchant accounts automate recurring charges so you're not manually invoicing every customer monthly.

- Your industry has high transaction volumes: If you're processing $100K+ monthly, the per-transaction savings from negotiating better merchant account rates (vs. using PayPal or Square) can save you $500 - $2,000/month.

- You want lower fees than all-in-one processors: PayPal and Square are easy to set up but charge 2.9% - 3.5% + $0.30 per transaction with no negotiation. A dedicated merchant account often gets you to 2.0% - 2.5% once you have volume.

| Pros | Cons |

| Essential infrastructure for accepting card payment | Transaction fees eat 1.5% - 3.5% of every sale |

| Enable e-commerce, in-person, and mobile transactions | Complex fee structures (tiered pricing can hide costs) |

| Payment gateways integrate with most platforms (Shopify, WooCommerce) | Chargeback fees ($15 - $50) add up if you have disputes |

| Recurring billing automates subscription revenue | ulti-year contracts with auto-renewal clauses are common |

| Fraud detection and chargeback management included | Automatic rollover can lock you into worse rates if you forget |

11. Ready to open your busines bank account?

There are obviously countless other bank account options out there. But these are the ones our banking experts recommend trying first.

And if you need help and expert consulation, you can always count on us, we can help you:

If you need help choosing the right bank and account type for your business stage, our experts help founders open accounts with a 98% success rate, using proven KYC frameworks and 10+ years of banking experience.

- Recommend the right bank and the right bank account for your needs;

- Support you in opening a reliable, trusted digital bank account or traditional bank account;

- Prepare necessary documents for account opening;

- Schedule an appointment with a Singapore bank representative;

- Monitor and assist in opening corporate bank accounts (physical and digital).

12. FAQs about types of business bank account

Look at monthly fees, minimum balance requirements, transaction limits, online banking features, and international transfer costs. If you operate globally, check multi-currency support. And most importantly: choose a bank that understands your business model.

- Keep it strictly for business.

- Do not use your personal bank account for business transactions.

- Use your business account to receive revenue and pay business expenses only.

This separation makes bookkeeping cleaner, tax filing easier, and protects you legally.

Ideally, the moment you open a company and plan to expand internationally.

An offshore account in Singapore, Hong Kong, or another financial hub helps you:

- Handle cross-border transactions smoothly

- Build trust with investors and partners

- Receive foreign payments efficiently

- Strengthen your global business presence

If you’re going international, having the right banking structure from day one is a smart move.

Bank transfers can sometimes take longer than expected due to several factors. These include batching or ACH processing times, the involvement of intermediary banks (especially for international transfers), and delays from external banks.

Additionally, transfers may be held for fraud detection checks (such as Anti-Money Laundering and Counter-Terrorism Financing regulations), or simply delayed bank holidays when financial institutions are closed.

If you want to learn more about each reason, and discover practical tips to speed up your transfers, check out our comprehensive guide: Why do bank transfers take so long? (+ How to speed them up).

With over a decade of experience serving as a trusted partner to more than 750 business owners seeking professional development and breakthroughs in the international market, we are an expert strategic corporate service provider helping you incorporate and operate successfully in 10 different countries

Our areas of expertise include:

- Strategic Consulting and Company formation in over 10 different countries worldwide such as Singapore, Hong Kong, the U.S., Australia, Thailand, Malaysia, and offshore destinations like BVI, Belize, Seychelles, and more.

- Account opening for personal and corporate bank accounts, as well as setting up PayPal and Stripe gateqays in countries like Singapore, Hong Kong, and the U.S..

- Tax Consulting and Preparation for SFRS IFRS financial reports, corporate income tax returns, VAT/GST (Value Added Tax/Goods and Services Tax), and more.

- Opreation support:

- Registered adress;

- Foreign consular legalization;

- Trademark and patent protection registration in Singapore and the US;

- Employment Pass application in Singapore and Hong Kong;

- Website design, international SIM number provision;

- DUNS registration.

With over 10 years of experience and a team of experts with 5 to 25 years of experience (international standard certifications) as well as direct partnerships with institutions such as OCBC, UOB, DBS, PayPal, and Stripe, we are proud to offer professional, legal, transparent, sustainable services with no hidden costs.

Global Link Asia Consulting Pte. Ltd. is pleased to announce the publication of the above insightful and informative article on our official website, Global Link Asia Consulting on 13th February 2026. The copyright for this article is exclusively held by Global Link Asia Consulting Pte. Ltd. Any unauthorized reproduction or distribution of this content without our express written permission is strictly prohibited. We value the protection of our intellectual property and appreciate your cooperation in adhering to these guidelines. Thank you for your continued support of Global Link Asia Consulting Pte. Ltd.