You may have noticed it takes a few days to transfer money to another bank. And it can take even longer if you transfer a lot of money.

So why is this the case, when you clearly see that purchases via internet banking show up within minutes?

Bank transfers don’t run on instant logic. They move through layered systems, checks, and intermediaries, each adding time:

- Is the transfer domestic or international?

- Does it pass compliance and fraud checks?

- Are multiple banks involved in the process?

To find these answers, banks rely on internal systems and external networks, many of which you don’t see. That’s where delays happen.

In this article, banking experts of Global Link Asia Consulting (GLAC) will break down why bank transfers take longer than expected. And more importantly, how to speed them up and avoid delays.

1. Reasons why bank transfers take so long (Expert insights)

Delays in bank transfers are rarely random. They usually come down to timing, systems, and risk checks. The good news is delays can be reduced, if you know how.

| Reasons for delayed bank transfers | Why does it take so long to transfer? | How to speed up? |

| Batching/ ACH payment (Automated Clearing House) | Banks process these in batches at fixed times during the day. | Send your transfer early in the morning (e.g. 8 AM) on a working day to catch the first processing batch. Missing the cutoff can delay your transfer by an entire day. |

| Intermediary banks | Your money pass through multiple banks before reaching the recipient. | Use banks or payment providers that support direct transfers to the destination country, receiving bank. |

| International transfer | Different countries, currencies, and time zones create extra processing layers. Currrencies are the most influential factor leading to extra processing time. | Transfer during overlapping business hours between both countries, ideally early in the day, to avoid overnight delays. Transfer using the same currency (USD, EUR, GBP) if possible. |

| External bank transfer | Transfers between different banks require additional clearing processes since each bank has its own policies | Whenever possible, transfer within the same bank (branches) or use instant transfer options if available. |

| Fraud detection (Money Laudering and Financing of Terrorism Prevention (ML/FT)) | Banks review transactions that appear unusual or high-risk. Your bank account could be frozen if it fails the fraud detection test | Keep your transfers consistent in amount and recipient, and ensure all details are accurate to avoid manual reviews. |

| Bank Holidays | Banks do not process transactions on non-working days | Always send transfers before weekends or public holidays, preferably in the morning on the last working day. |

Why it is slow

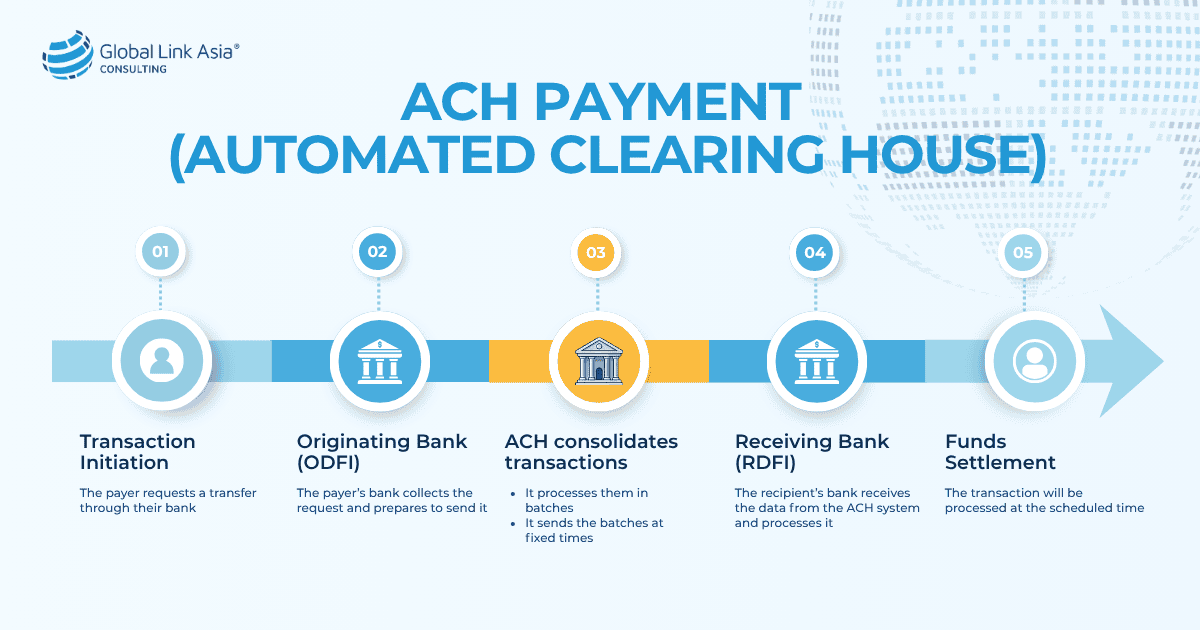

An ACH payment is a type of electronic bank transfer that runs through the Automated Clearing House network. Instead of moving money instantly, this system is designed for efficient, high-volume processing.

For example, in the United States, these transactions are governed by Nacha, the organization that sets the rules for the ACH network.

ACH and similar clearing systems don’t process transactions in real time. Instead, banks group payments into batches and send them at fixed intervals during the day.

Here’s how it works in practice:

- Funds move from the payer’s account to the recipient’s account through two banks:

- The Originating Depository Financial Institution (ODFI);

- The Receiving Depository Financial Institution (RDFI).

- Payments are not processed one by one. Instead, banks group transactions into batches and send them at fixed times during the day.

ACH payment (Automated Clearing House)

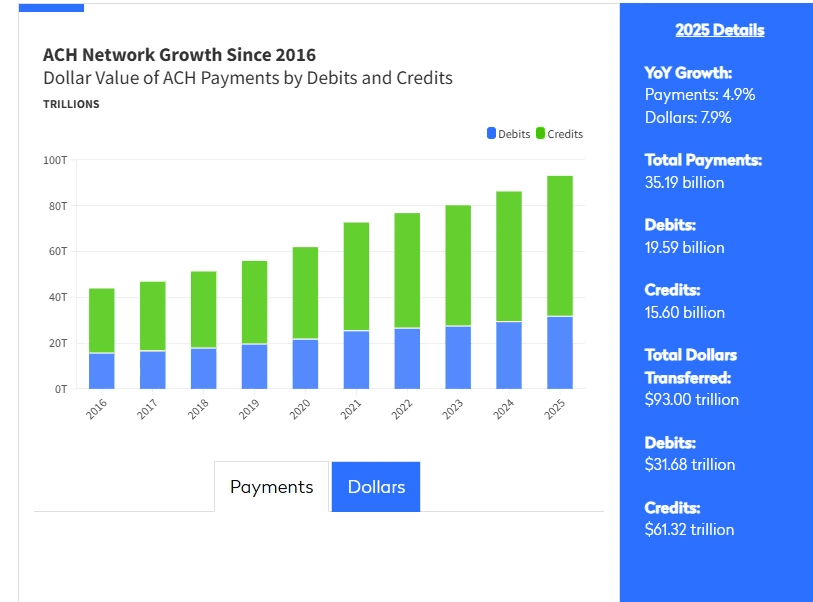

At scale, this system is extremely powerful. In a report by NACHA, Overall ACH Network Volume 2025 alone, Same Day ACH payment volume reached 1.4 billion payments for the year, valued at $3.9 trillion.

ACH Network Growth since 2016: Source: Nacha

However, this system creates a hidden delay: If your transfer arrives after the cutoff time, it doesn’t get processed immediately — it simply waits for the next batch cycle. In practice, that can mean a delay of several hours, v.v or an entire business day.

How to speed up

Timing is everything here. Send your transfer at the end of the previous day aroud 4PM or early in the morning (around 8 AM) of a working day to catch the first processing batch.

This gives your payment the maximum chance to move through the system on the same day.

If you send late in the afternoon, you’re effectively choosing to wait.

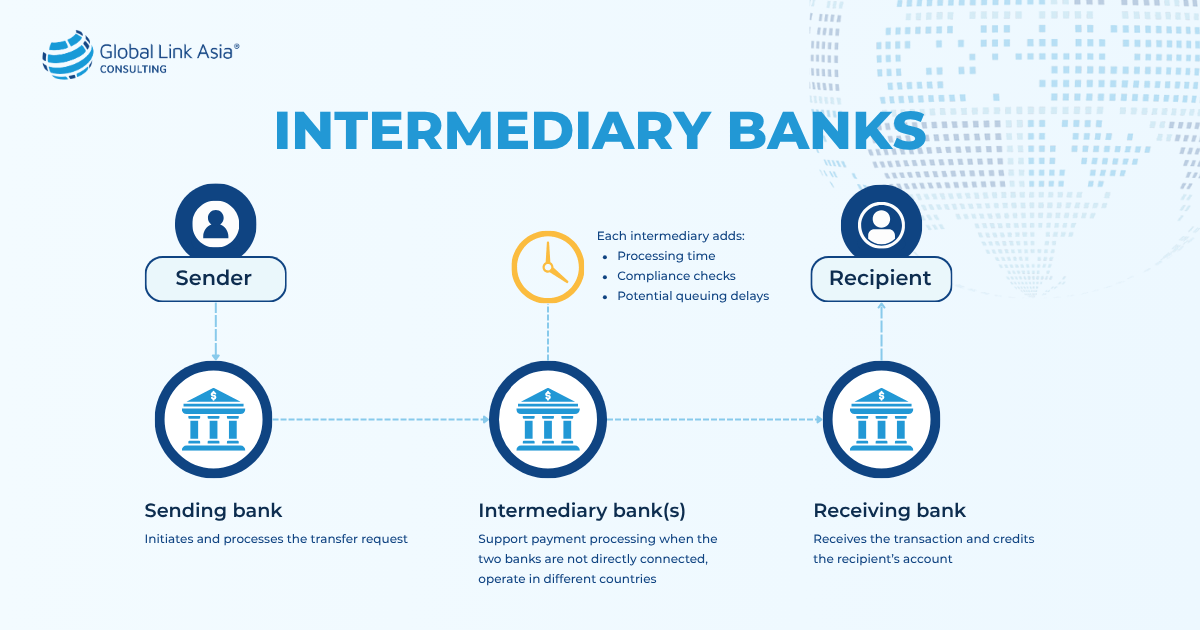

Not all banks are directly connected. In some cases, one or more Intermediary banks help process the payment, especially if the two banks are banks from different countries with no direct relationship or they are dealing with different currencies. This can affect how long the transfer takes and how much it costs.

Each intermediary adds:

- Processing time;

- Compliance checks;

- Potential queuing delays.

Intermediary banks

The result? A transfer that looks simple on the surface can involve multiple hidden steps behind the scenes. In addition, intermediary banks are also one of may reasons your payments do not received in full amount.

How to speed up

Choose banks or payment providers that offer direct transfer corridors to your destination country.

Fintech platforms and international banking solutions often optimize this by minimizing or bypassing intermediaries.

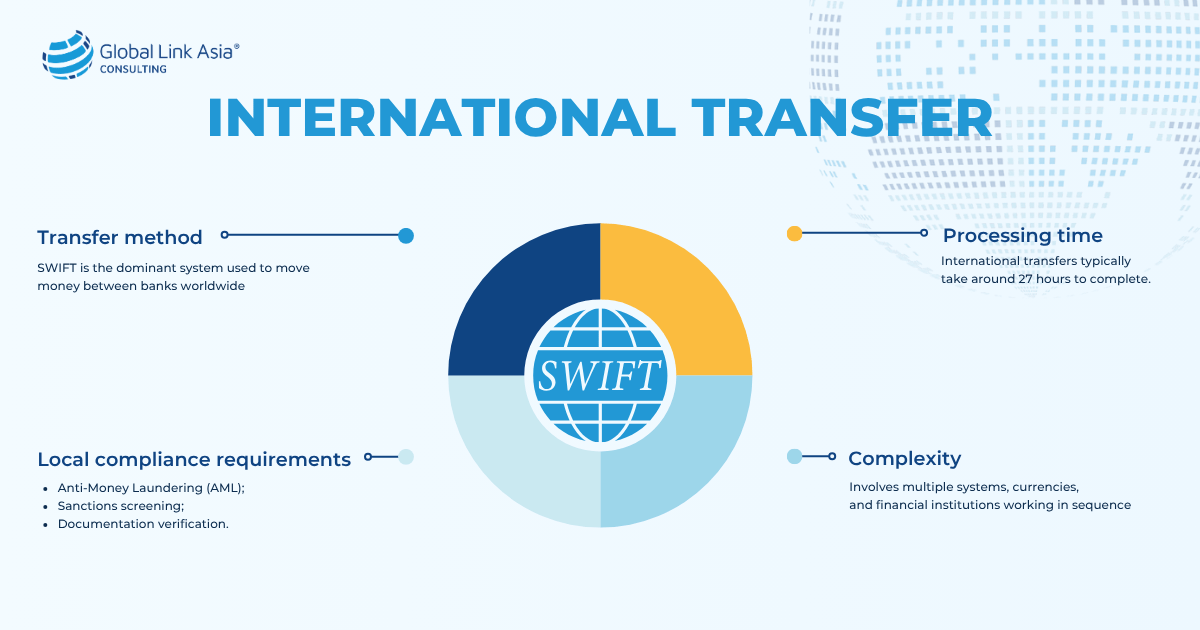

Cross-border transfers look simple on the surface, money moves from one country to another.

In reality, they involve multiple systems, currencies, and institutions working in sequence.

In the international transfer domain, a SWIFT transfer is the dominant messaging system used to transfer money from one bank to another accross countries.

Even with a system of interconnected banks within the SWIFT system, a report of Statrys showed that SWIFT transfers typically take around 27h to transfer money

International transfer

Here’s where the complexity of international transfer comes from:

- Different banking systems: Each country operates on its own infrastructure, processing timelines, and settlement rules;

- Time zone differences: Your bank may process the payment instantly, but the receiving bank could be offline or outside business hours;

- Local compliance requirements: Cross-border transfers often go through additional checks (AML, sanctions screening, documentation review), which can pause the transaction.

But the biggest hidden factor is currency conversion.

When a transfer involves two currencies, it’s no longer just a payment.

It becomes a multi-step financial process:

- Foreign exchange (FX) pricing and execution: The bank must determine the exchange rate and execute the currency trade.

- Liquidity sourcing: Funds may need to be sourced through correspondent banks to match the required currency.

- Multi-currency settlement: The transaction must settle across two separate currency systems, not just one.

How to speed up

You can’t remove the complexity of international transfers — but you can reduce friction at every step.

Our banking experts offer you 3 tips to help you make international transfers faster

| Tips | Details |

| Send in the right time window | Timing matters more than most people think.

→ This ensures your payment doesn’t sit idle waiting for the receiving system to open. |

| Minimize currency conversions | To reduce delays:

→ Fewer conversions = fewer processing steps. |

| Use banks with strong correspondent networks | Not all banks are equal in cross-border transfers.

You should consider opening an account with estemmed bank in financial centers such as the U.S (J.P. Morgan, Chase Bank), Singapore ( UOB, DBS, OCBC), Hong Kong (HSBC, Bank of China) |

Transfers within the same bank are fast because everything happens inside a single, controlled system.

The bank already holds both accounts, so it can instantly update balances without needing to “ask” anyone else.

But the moment you send money to another bank, the process changes completely.

The transaction now has to move through interbank clearing networks, where multiple institutions must coordinate before funds are finalized.

Here’s what actually happens behind the scenes:

- Your bank sends the payment instruction out to the network;

- The receiving bank validates the details and confirms the account;

- Clearing systems reconcile balances between the two institutions;

- Settlement occurs, sometimes immediately, but often in scheduled cycles.

Each of these steps introduces latency.

How to speed up

If you want to speed up bank transfers, you can consider these 2 approaches:

Stay within the same bank when possible

- Transfers within the same bank are usually instant or near-instant;

- No clearing, no intermediaries, no settlement delays.

→ If speed is critical, this is always the fastest option.

Many countries now support real-time payment networks that bypass traditional clearing delays.

Examples globally include:

- Faster Payments (UK);

- UPI (India);

- Real-time rails in Singapore and the EU.

These systems:

- Process payments 24/7;

- Settle within seconds or minutes;

- Reduce dependency on batch cycles.

→ If your country supports it, this is the best alternative to same-bank transfers.

Why it’s slow

Banks are not just processing payments they are also responsible for preventing financial crime.

Every transaction is screened under Money Laundering and Terrorism Financing (ML/FT) regulations, using automated systems and, in some cases, manual review.

This is where delays can become unpredictable.

Here’s what typically triggers a review:

- Unusual transaction patterns: Sudden large transfers, new recipients, or activity that doesn’t match your history;

- High-risk jurisdictions or industries: Certain countries or business types require enhanced scrutiny;

- Inconsistent or incomplete information: Missing payment purpose, unclear sender/receiver details;

- Regulatory flags: Sanctions screening, AML checks, or internal risk scoring.

When a transaction is flagged:

- It may be paused for manual review;

- Additional documents may be requested;

- In rare cases, accounts can be temporarily restricted or frozen.

On top of that, banks may need to respond to external regulatory inquiries or government checks, which adds another layer of delay outside their direct control.

For example, according to the federal law in the United States, federal law requires banks to report any cash transactions over $10,000 made by or for one person.

This also includes multiple transactions that add up to more than $10,000 within a single day.

Filing obligation in the U.S for transaction more than 10,000 USD

How to speed up (and avoid delays)

You can’t bypass compliance, but you can make your transactions low-risk and easy to approve.

| Tips | Details |

| 1. Keep transaction patterns consistent | Banks build a “behavior profile” over time.

→ Consistency reduces the chance of triggering alerts. |

| 2. Ensure all details are complete and accurate | Small errors create big delays:

→ Clean data = faster automated approval. |

| 3. Avoid sudden, unexplained changes | Red flags include:

→ If needed, inform your bank in advance for large or unusual payments. |

Why it’s slow

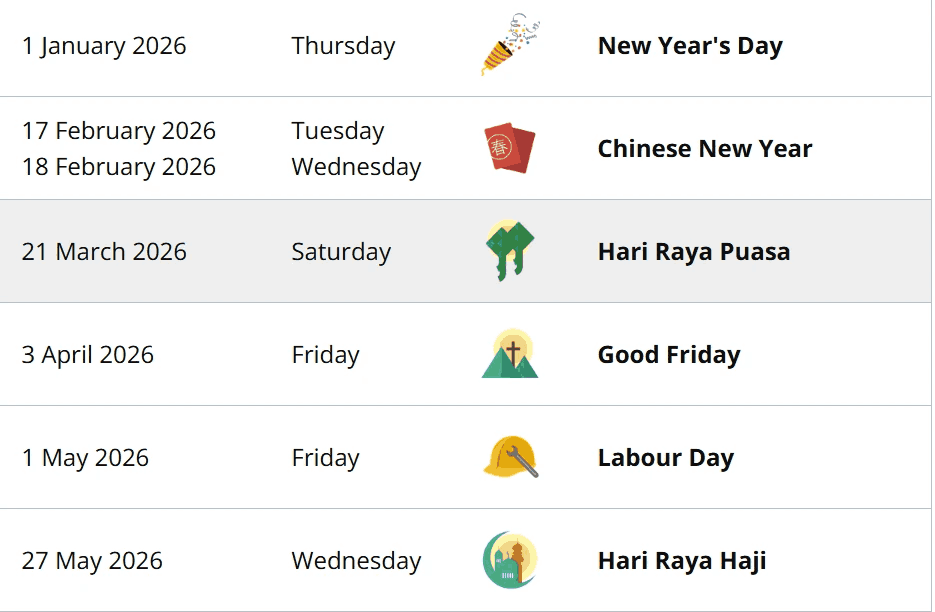

Banks do not process transactions on non-working days, and that includes weekends and public holidays.

This might sound obvious, but in practice, it creates hidden delays that many people underestimate.

Here’s what actually happens:

- If you send a transfer on a bank holiday, it doesn’t start processing;

- It simply sits in the queue until the next working day;

- If multiple non-working days stack (e.g. weekend + holiday), the delay compounds.

For example:

- If you send on Friday evening, the transfer is processed on Monday;

- If Monday is a holiday, the transfer is processed on Tuesday.

Look out for holidays when sending money (Source: Ministry of Manpower Singapore)

For international payments, the effect is amplified: Your bank in your country may be working. But the receiving bank in your partner’s country may be on holiday. Your bank sends the payment. But the receiving bank is closed and cannot process it This creates a silent delay in the middle of the transaction.

In some cases, intermediary (correspondent) banks may also be in different regions with their own holiday schedules.

How to speed up

| Tips | Details |

| 1. Always check both countries’ calendars | For cross-border payments:

|

| 2. Send before the holiday starts |

This ensures your payment enters processing before systems shut down. |

2. Make your payments move faster

Payment delays are not random. They are the result of how the system is built, batching cycles, interbank networks, FX layers, compliance checks, and non-working days.

You already know where delays come from. Now it’s about turning that knowledge into a system that ensures your money moves as fast as your business does.

If you need support, our banking experts can help you:

If you need help choosing the right bank and account type for your business stage, our experts help founders open accounts with a 98% success rate, using proven KYC frameworks and 10+ years of banking experience.

- Choose the right banking options for your needs;

- Open both personal and business bank accounts;

- Build a structure that supports faster, more reliable transactions.

3. FAQs about why bank transfers take so long

SWIFT is a global financial messaging network, not a payment system. It allows banks to securely exchange payment instructions, often within seconds.

Even when everything looks correct, several behind-the-scenes factors can slow things down:

- Regulatory compliance checks: Every transfer is screened for fraud, AML, and sanctions. If flagged, it may be paused or manually reviewed;

- Country-specific controls: Some countries have stricter rules. For example, transfers to India can take longer due to approval requirements;

- Technology limitations: Not all banks use real-time systems. Legacy infrastructure often means batch processing or manual steps;

- Bank size and capabilities: Larger banks tend to process faster thanks to better systems and fewer intermediaries.

With over a decade of experience serving as a trusted partner to more than 750 business owners seeking professional development and breakthroughs in the international market, we are an expert strategic corporate service provider helping you incorporate and operate successfully in 10 different countries

Our areas of expertise include:

- Strategic Consulting and Company formation in over 10 different countries worldwide such as Singapore, Hong Kong, the U.S., Australia, Thailand, Malaysia, and offshore destinations like BVI, Belize, Seychelles, and more.

- Account opening for personal and corporate bank accounts, as well as setting up PayPal and Stripe gateqays in countries like Singapore, Hong Kong, and the U.S..

- Tax Consulting and Preparation for SFRS IFRS financial reports, corporate income tax returns, VAT/GST (Value Added Tax/Goods and Services Tax), and more.

- Opreation support:

- Registered adress;

- Foreign consular legalization;

- Trademark and patent protection registration in Singapore and the US;

- Employment Pass application in Singapore and Hong Kong;

- Website design, international SIM number provision;

- DUNS registration.

With over 10 years of experience and a team of experts with 5 to 25 years of experience (international standard certifications) as well as direct partnerships with institutions such as OCBC, UOB, DBS, PayPal, and Stripe, we are proud to offer professional, legal, transparent, sustainable services with no hidden costs.

Global Link Asia Consulting Pte. Ltd. is pleased to announce the publication of the above insightful and informative article on our official website, Global Link Asia Consulting on 25th March 2026. The copyright for this article is exclusively held by Global Link Asia Consulting Pte. Ltd. Any unauthorized reproduction or distribution of this content without our express written permission is strictly prohibited. We value the protection of our intellectual property and appreciate your cooperation in adhering to these guidelines. Thank you for your continued support of Global Link Asia Consulting Pte. Ltd.