Most founders in Singapore assume audits are only for big corporations. They’re not.

At the same time, many small companies think they’re automatically exempt. That’s not always true either.

Every year, directors of companies registered with Accounting and Corporate Regulatory Authority get confused about whether they qualify for audit exemption, and what happens if they get it wrong.

- Penalties, compliance issues, unnecessary costs.

- Or worse: non-compliance without even knowing it.

A very good question from a confused business owner

In this guide, we partnered with an expert (our long-term audit partner) to show you when a Singapore company needs an audit, or simply a one-stop tax-accounting package is enough.

No jargon. No guesswork. Just clear explanations from an expert perspective, plus a practical checklist you can use to check at the end of our article.

First, we need to understand what the definition of auditing is.

1. What is auditing in Singapore according to ACRA and IRAS?

1.1. What is auditing?

In Singapore, a company audit is a formal, independent examination of a company’s financial statements to determine whether they give a “true and fair view” of its financial position.

Under the Accounting and Corporate Regulatory Authority (ACRA), audits are governed by the Companies Act (CA) Division 2 Audit and other Admendments. The Act sets out:

- When a company must appoint an auditor;

- The duties and powers of auditors;

- Which companies qualify for audit exemption;

- Directors’ responsibilities for preparing financial statements.

Audit regulation in the Companies Act of Singapore

From a tax perspective, the Inland Revenue Authority of Singapore (IRAS) IRAS relies on accurate financial statements to assess corporate income tax. If your accounts are audited, it increases credibility and reduces tax risk exposure.

1.2. What is an auditor?

An auditor’s role is not to prepare your accounts, but to independently review them and express an opinion on whether they comply with Singapore Financial Reporting Standards (SFRS).

An auditor’s role is not to prepare your accounts, management is responsible for that.

Instead, the auditor independently reviews the financial statements and reports on whether they:

- Comply with financial reporting standards (such as SFRS); and

- Provide a true and fair view of the company’s financial position and performance.

The auditor’s report must be attached to (or endorsed upon) the financial statements when these statements are presented to shareholders at the company’s Annual General Meeting (AGM).

Whether your company needs one depends on size, revenue, and exemption criteria, which we’ll break down next.

2. Singapore statutory audit requirements

Under the Companies Act, all companies (unless exempted) must undergo an annual statutory audit.

The requirement of fully and duly audited financial statements of companies in Singapore

A statutory audit is:

- An independent examination of financial statements;

- Conducted by a licensed public accountant/accounting firm;

- Required by law (unless exempted).

In Singapore, only public accountants or accounting firms approved by the Accounting and Corporate Regulatory Authority (ACRA) are allowed to act as company auditors.

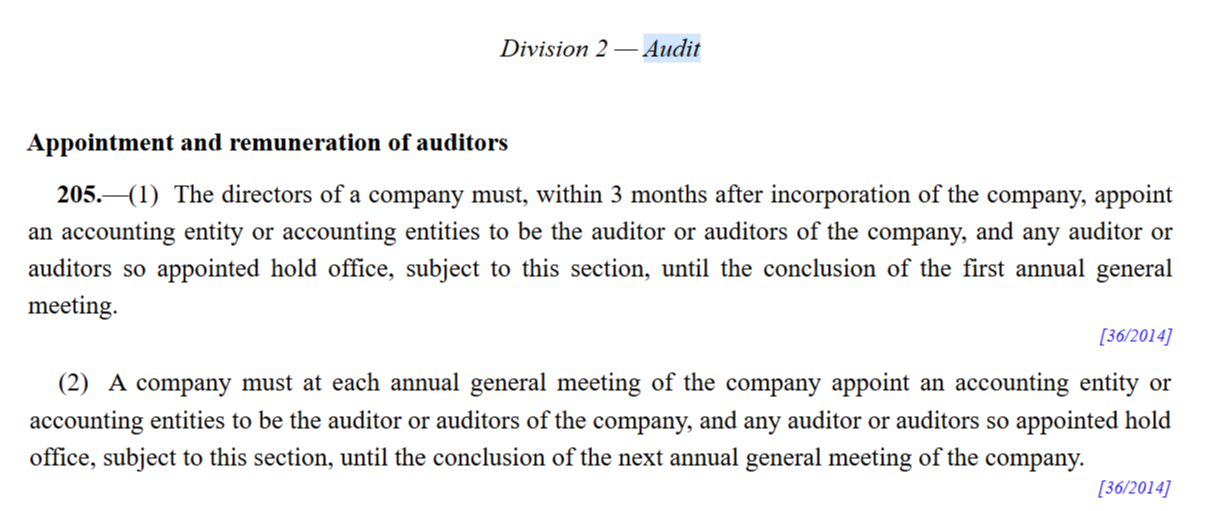

Directors are legally required to

- Appoint at least one accounting entity as auditor;

- Do so within 3 months of incorporation.

Once appointed, the auditor holds office:

- From the date of appointment;

- Until the conclusion of the company’s next Annual General Meeting (AGM).

For newly incorporated companies:

- The first appointed auditor serves until the first AGM;

- At the first AGM, shareholders must either reappoint the same auditor or appoint a new one;

- The appointed auditor then serves until the conclusion of the next AGM.

And this cycle continues annually.

If directors fail to appoint an auditor:

- Any company member can apply to ACRA;

- ACRA may appoint an auditor on behalf of the company.

In other words, you cannot simply ignore the requirement.

3. Audit Exemption in Singapore (ACRA Guidelines)

Even if a company qualifies for exemption, ACRA may still require audited financial statements if the company breaches laws relating to:

- Keeping proper accounting records (Section 199 CA);

- Laying financial statements at AGM (Section 201 CA).

At this point, you’re probably wondering:

If all companies must undergo an audit unless exempted, then what exactly qualifies as audit exemption in Singapore under ACRA guidelines?

Good question.

Because this is where most directors get confused, and where many companies either overpay for unnecessary audits or accidentally fall into non-compliance.

Let’s break down how audit exemption works in Singapore, based on ACRA’s official criteria.

An entrepreneur of a Singapore company struggle with ACRA’s audit requirements

Not every company in Singapore needs to be audited.

Under the Companies Act regulated by Accounting and Corporate Regulatory Authority (ACRA), a company is exempt from audit if it qualifies as:

- A small company;

- Part of a small group;

- A dormant company.

Let’s break each one down clearly.

A company qualifies as a small company if:

- It is a private company in the relevant financial year; and

- It meets at least 2 out of 3 criteria for the immediate past two consecutive financial years.

| Criteria | Threshold |

| Total annual revenue | ≤ S$10 million |

| Total assets | ≤ S$10 million |

| Number of employees | ≤ 50 |

For example, let’s say you have a ABC Pte.Ltd in Singapore; the company has

- Revenue: S$6 million;

- Total assets: S$8 million;

- Employees: 32.

It meets all 3 criteria for the past two years; therefore, ABC qualifies as a small company, so no audit is required.

If your company is part of a corporate group:

- The company itself must qualify as a small company; AND

- The entire group must qualify as a small group on a consolidated basis.

It meets at least 2 of the 3 criteria (same thresholds above) on a consolidated basis (They need to have consolidated financial statements) for the past two consecutive financial years.

| Criteria | Threshold |

| Total annual revenue | ≤ S$10 million |

| Total assets | ≤ S$10 million |

| Number of employees | ≤ 50 |

For example, let’s say you have a parent company and 2 subsidiaries in Singapore in Singapore; the company has consolidated figures as follows:

- Revenue: S$9 million;

- Total assets: S$11 million;

- Employees: 45.

This group meets 2 out of 3 criteria for the past two years, so no audit is required.

A company is exempt if it is dormant, meaning:

- It has been dormant since incorporation; OR

- It has been dormant since the end of the previous financial year.

A company is dormant if no accounting transactions occur during the period.

However, the following do not count as accounting transactions:

- Appointment of a company secretary;

- Appointment of an auditor;

- Maintaining company registers;

- Paying statutory government fees.

For example, XYZ Pte Ltd was incorporated but has:

- No revenue;

- No expenses;

- No business activity;

- It only paid ACRA filing fees.

It is considered dormant, so no audit required. But once any accounting transaction occurs (e.g., sales, expenses, salary payment), it ceases to be dormant and the audit requirement applies unless exempted

4. How to choose an audit firm/auditor in Singapore?

If you’ve ever wondered how to choose the right audit firm in Singapore, it usually comes down to two core factors:

- Regulatory credibility;

- Operational fit.

Let’s talk about compliance and competence. Plus, we’ll break down what actually separates a reliable auditor from a risky one.

| Criteria | Key Considerations |

| Regulatory credibility | Start with the basics. In Singapore, only public accountants or accounting firms approved by the Accounting and Corporate Regulatory Authority (ACRA) can act as statutory auditors. You must check their info and their lisence. That’s non-negotiable. |

| Industry & Business Fit | Not all audit firms are built the same. Some specialize in:

The right audit firm should understand:

|

| Responsiveness & Process Transparency | An audit shouldn’t feel chaotic. A strong audit firm will:

If they can’t explain adjustments clearly, that’s a red flag. |

| Fee structure | Yes, fees matter. But choosing the cheapest audit firm can cost more in the long run. Instead, look for:

A professional firm will justify its fees based on complexity, not guesswork. |

5. Final takeaway: Do your Singapore company need an audit

- Do you need an audit?

- Are you eligible for exemption?

- Have you appointed an auditor?

- Are your financial statements compliant?

By now, you’ve seen the full picture:

- What a statutory audit is;

- What Singapore statutory audit requirements say;

- Who qualifies for audit exemption.

Under the Companies Act regulated by Accounting and Corporate Regulatory Authority (ACRA), the default rule is simple:

All companies must be audited — unless they qualify for exemption. So instead of guessing, use our simple and quick compliance checklist.

| Question | What to Check |

| Do you need an audit? | Are you a private company that does NOT qualify as a small company, small group, or dormant company? |

| Are you eligible for exemption? | Do you meet at least 2 of 3 criteria (≤ S$10m revenue, ≤ S$10m assets, ≤ 50 employees) for the past 2 consecutive financial years? |

| If part of a group, are you eligible as a small group? | If part of a group: Does the entire group meet 2 of 3 criteria on a consolidated basis? |

| Are you eligible for exemption as a dormant company? | Are you dormant (no accounting transactions)? |

| Have you appointed an auditor? | If audit is required, was an auditor appointed within 3 months of incorporation OR immediately when exemption criteria are no longer satisfied? |

| Even if you qualify for exemption: | ACRA may still require audited financial statements if your company breaches laws relating to:

Audit exemption does not mean compliance exemption. |

6. How can we help you with your company audit?

If you need a trusted partner to guide your SME through audit requirements — especially if you’re a growing business navigating exemption thresholds — you don’t have to figure it out alone.

At Global Link Asia Consulting, we work closely with experienced, certified auditors, audit firms, and licensed public accountants approved by Accounting and Corporate Regulatory Authority (ACRA).

That means:

- Clear assessment of whether you need an audit;

- Proper auditor appointment (if required);

- Structured, smooth audit coordination;

- A personalized solution that fits your business model.

Whether you’re a small company, part of a group, or scaling beyond exemption limits, we help you stay compliant — without unnecessary stress or overpaying for services you don’t need.

7. FAQs about audit Requirements for Singapore Companies

Yes, a company auditor can be removed by:

- Passing a resolution at a general meeting;

- With special notice given.

But this must follow proper statutory procedure

Audited financial statements in Singapore are financial reports that have been independently examined by a licensed public accountant to confirm that they:

- Comply with Singapore Financial Reporting Standards (SFRS); and

- Present a true and fair view of the company’s financial position and performance.

They typically include:

- Statement of Financial Position (Balance Sheet);

- Statement of Profit or Loss;

- Cash Flow Statement;

- Statement of Changes in Equity;

- Notes to the Financial Statements;

- The Auditor’s Report.

Under the Companies Act regulated by Accounting and Corporate Regulatory Authority (ACRA), companies that do not qualify for audit exemption must prepare and present audited financial statements at their AGM.

Yes. They are completely different.

Many directors confuse the two, but they serve different purposes and are conducted by different authorities.

| Category | Company Audit (Statutory Audit) | IRAS Audit |

| Definition | A legal requirement under the Companies Act. Conducted by an independent auditor. Required before submitting financial statements to Accounting and Corporate Regulatory Authority (ACRA), if the company is not audit-exempt. | An IRAS audit is conducted by the Inland Revenue Authority of Singapore (IRAS). This is a tax enforcement or compliance review. It can happen even if your company is audit-exempt. And even if your financial statements were audited. |

Purpose | To confirm that your financial statements comply with reporting standards and present a true and fair view. This is part of your annual corporate compliance. It happens every year (if required). | IRAS may audit a company to:

|

We offer a comprehensive range of accounting and tax services for Singaporean companies. Our services include:

- Tax Consulting including corporate income tax, GST tax, contractor tax, and more.

- Monthly/Annual Tax Accounting services in accordance with Singapore accounting standards (SFRS).

- QuickBooks Consulting and Licensing.

- Corporate Income Tax Return Preparation

- GST Tax Return Preparation.

5.0 / 5.0 Reviews

Global Link Asia Consulting Pte. Ltd. is pleased to announce the publication of the above insightful and informative article on our official website, Global Link Asia Consulting on 02nd March 2026. The copyright for this article is exclusively held by Global Link Asia Consulting Pte. Ltd. Any unauthorized reproduction or distribution of this content without our express written permission is strictly prohibited. We value the protection of our intellectual property and appreciate your cooperation in adhering to these guidelines. Thank you for your continued support of Global Link Asia Consulting Pte. Ltd.