If you still think opening a bank account in Hong Kong is not possible for foreigners, you are wrong.

Foreigners can open a bank account in Hong Kong. Foreign company can open a corporate bank account in Hong Kong.

The problem here is not about knowing you can open one, but how you can successfully open and actually use your Hong Kong bank account for your company and personal daily life.

In this comprehensive guide, our banking expert will show you:

- What banks really care about;

- What mistakes to avoid;

- And how to increase your chances of bannk application approval from the start.

But first, let’s look at reason why foreigners look into ways to open a bank account in Hong Kong.

1. Why you need to open a bank account in Hong in the first place?

1.1. Protect your assets through diversification

One of the key reasons our banking experts always recommend opening a Hong Kong bank account is asset protection.

The advice is clear: Don’t keep all your money in one place. Instead, have a back-up bank account.

Because this helps you reduce hidden risks such as:

- Unexpected account freezes or closures;

- Changes in government policies;

- Banking restrictions;

- Sudden economic shocks.

A Hong Kong bank account gives you a stable and internationally recognized place to hold funds, often in multiple currencies.

Expert recommendation from GLAC

From our experience working with international entrepreneurs and business owners, we always recommenend a simple but powerful principle: never rely on just one bank account.

At a minimum, you should maintain:

- At least 2 bank accounts;

- A combination of 1 account from lisenced digital banks (from Singapore or other countries) and 1 account from traditional physical banks.

In practice, we’ve seen many cases where businesses or individuals faced challenges simply because their funds were concentrated in one account or one banking system.

That’s why we guide our clients to build a more resilient structure, combining the flexibility of digital banks with the stability of traditional banks.

1.2. Easy for international transactions

If you travel frequently across Asia, including Hong Kong, mainland China, Hong Kong, South Korea, Japan, and Thailand , a Hong Kong bank account makes life much easier.

You can manage payments across different countries without constantly converting money or relying on third-party apps.

A Hong Kong account also gives you access to a debit /credit card and multi-currency payments. In this way, A Hong Kong bank account allows you to operate across multiple markets with ease.

You can:

- Hold different currencies in one account;

- Receive payments from international clients;

- Pay suppliers and partners worldwide.

It’s especially useful if you’re an entrepreneur or business owner who needs to move quickly and manage money across borders.

Manage your savings across different currencies and earn interest on your account balance with a saving account from HSBC Hong Kong

1.3. Easy payments to Chinese suppliers

If you run a business like dropshipping, e-commerce, or work with suppliers in China, a Hong Kong bank account is a big advantage.

Transferring money from Western or European accounts to China can be complicated, slow, and sometimes restricted.

But with a Hong Kong account, payments to Chinese suppliers are much smoother and more efficient. This makes your supply chain faster and easier to manage.

1.4. Better access to payment gateways

If you’re running an e-commerce business, payment gateways are essential.

In many countries, it’s difficult to access global payment systems like Stripe or PayPal.

A Hong Kong company with a Hong Kong bank account can help you:

- Open global payment gateways more easily

- Accept international credit and debit card payments

- Serve customers in the US, Europe, and other markets

This gives you a more professional and scalable payment setup for your business.

2. What Hong Kong banks really care about?

When it comes to opening a bank account in Hong Kong, banks don’t just look at whether you submit the right documents. They focus on who you are and how you operate.

From our banking expert’s 10-year experience GLAC, they evaluate applications from two key angles:

- Who qualifies to open an account?

- How do bankers and banks perceive your level of trustworthiness?

2.1. Who qualifies to open an account at a Hong Kong bank?

Banks want to understand your background, where you live, where your business is based, and how you are connected to Hong Kong.

They generally do not limit applications based on nationality or where you currently live. Foreigners, including company directors, shareholders, expats, digital nomads, and frequent travelers, can apply and open accounts.

However, if you are from a blacklisted or high-risk country on the bank’s internal list, approval becomes extremely difficult. It is impossible to open an account.

Foreigners, which are often non-residents or non-permanent residents, can open accounts. However, the level of scrutiny is higher, and your business substance and purpose must be clear.

What is the difference between residents and non-residents in Hong Kong when opening a bank account?

For residents, banks already have a clear track record, such as local address, income history, and employment in Hong Kong. This makes the review process faster and simpler.

For non-residents, the bank has no local history to rely on. As a result, they need to conduct deeper checks, sometimes verifying with your existing banks or reviewing your financial background more carefully.

This process can take more time and involve more documentation, as the bank needs to fully understand and assess your risk profile before approving the account.

2.2. How do bankers and banks perceive your level of trustworthiness?

Traditional banks usually require a physical meeting. You often need to visit the bank in person so they can verify your identity and assess your application directly. This is part of their strict due diligence process.

Beyond residency and physical meeting (for traditional banks), banks assess your application through your documents and business profile. This includes your company structure, source of funds, business activities, and supporting paperwork.

Banks follow two key processes:

KYC (Know Your Customer) documents include, but are not limited to:

- Passport or ID;

- Proof of address;

- Source of funds;

- Personal background and financial history;

- Purpose of opening the account;

KYB (Know Your Business) documents include, but are not limited to:

- Company registration documents;

- Business plan and activities;

- Shareholder and director details;

- Financial statements or transaction flow;

- Source of business funds.

If your profile looks clear, consistent, and low-risk, your chances of approval are significantly higher. If there are gaps or unclear points, banks are likely to reject the application.

3. Our number 1 suggestion to increase your chance of account application approval

Avoid links to high-risk or blacklisted countries, and ensure your activities comply with AML (Anti-Money Laundering) and CTF (Counter-Terrorism Financing) standards.

Simple and well-structured business models with clear fund sources and transaction flows, and a history of doing business are easier for banks to review and approve.

To illustrate our point, here is a case study of two business owners before they came to us. Our banking experts reviewed their situations and identified the reasons why their applications failed in the first place.

3.1. Case study 1: High-risk business model

An international client applied for a Hong Kong bank account with a business focused on AI tools combined with digital tokens.

At first glance, the business looked innovative. However, during our GLAC internal review, we raised concerns about:

- The use of digital tokens;

- Lack of clear regulatory classification;

Because the business model was complex and not easy to clearly explain, the application was declined.

Key takeaway: If a business involves new emerging technologies like AI or digital tokens, it must be extremely clear, well-documented, and compliant with regulations to reduce perceived risk.

3.2. Case Study 2: Shipping policy with restricted countries

Another client ran an e-commerce business with a global shipping policy on their website stating that they ship everywhere.

Our banking experts see that as potential concerns during the bank's reviews due to:

- Potential exposure to sanctioned or restricted jurisdictions;

- Difficulty in monitoring transaction flows;

- Increased CTF (Counter-Terrorism Financing) and compliance risk.

After adjusting the policy to clearly exclude restricted countries, showing the list of countries they ship to, and improving compliance transparency, the application had a much higher chance of approval.

Key takeaway: Your business policies (like shipping, payments, or customer regions) must be clearly defined and compliant. Banks need to see that you are not operating in or serving high-risk areas.

In both cases, the issue was not the business itself, but how clearly the risk and compliance aspects were presented to the bank.

4. Types of Hong Kong bank accounts available for foreigners

Hong Kong banks offer various types of accounts depending on your needs. The 6 banks account foreigners can open are:

| Options | Who should open |

| Corporate account | Entrepreneurs, business owners. |

| Savings account | Foreign professionals and international students. |

| Multi-currency account | Expatriates, freelancers, or businesses transacting in multiple currencies. |

| Current account | Professionals who require cheque-writing, high-frequency transactions. |

| Priority banking account | High-net-worth individuals in need of wealth management, exclusive investment opportunities, and access to dedicated relationship managers. |

| Bank account with Hong Kong digital banks | Hong Kong residents with their Hong Kong Identity Card. |

5. Popular banks for foreigners to open a bank account

With a renowned reputation and presence all over the world, some local and international are capable of providing account options tailored for foreigners.

At the momment, digital banks in Hong Kong are only an option for companies with local Hong Kong resident directors and shareholders, as their eligibility process often requires a Hong Kong Identity Card, so in this guide, we will not show any digital banks recommendation.

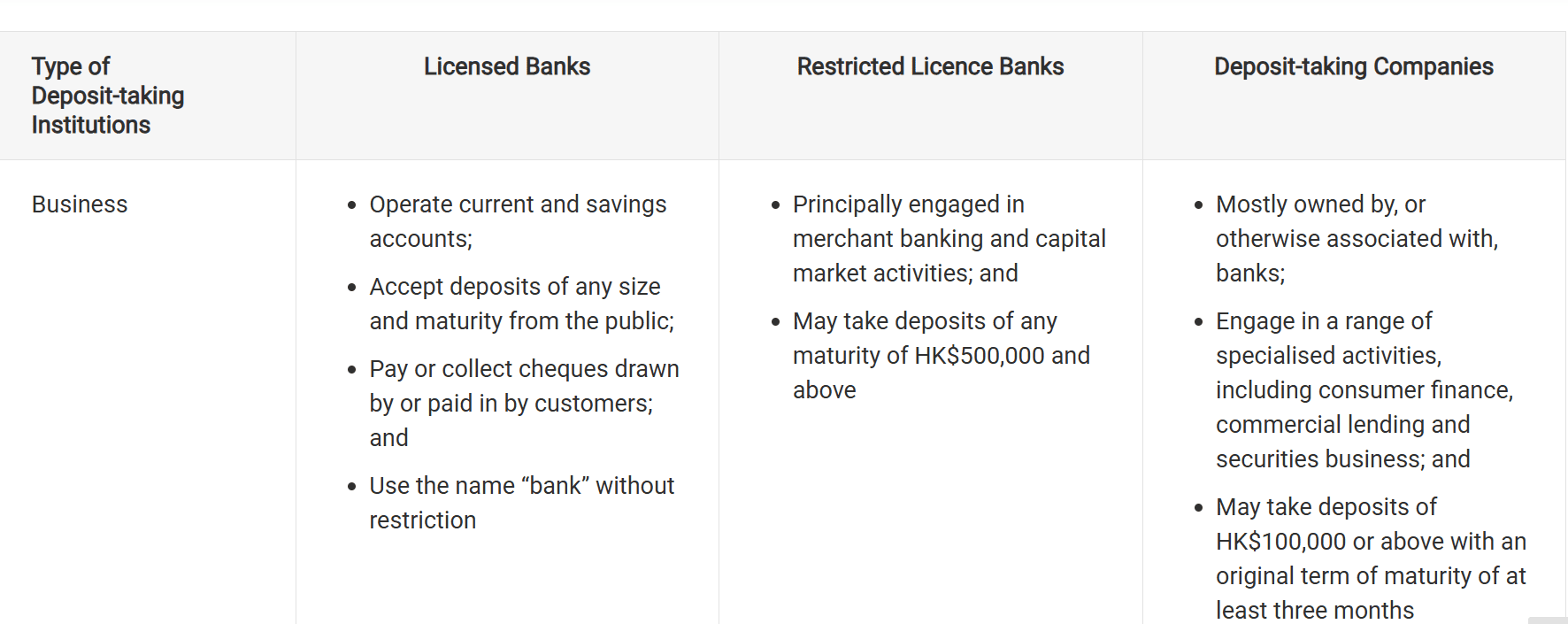

Hong Kong’s banking system is structured into three tiers, each serving different needs and levels of regulation. At the top are licensed banks, which offer full banking services such as corporate accounts, lending, and international transactions (e.g. HSBC, Standard Chartered).

The second tier is restricted licenced banks, which mainly focus on investment and capital market activities, typically serving larger corporates.

The third tier includes deposit-taking companies, which operate on a smaller scale, often providing specialized financing services.

In this guide, we’ll walk through examples of each tier to help you understand which type of bank best fits your business needs.

Banks regulated under the Hong Kong Monetary Authority

- Bank of China (Hong Kong) Limited;

- Hongkong and Shanghai Banking Corporation Limited (HSBC); and,

- Citibank (Hong Kong) Limited.

- J. P. Morgan Securities (Asia Pacific) Limited;

Goldman Sachs Asia Bank Limited;

- BPI International Finance Limited; and,

Chong Hing Finance Limited.

6. How can a foreigner open a bank account in Hong Kong?

Banking tip from expert

In Hong Kong, traditional banks implement stringent Know Your Customer (KYC) processes that can make account opening more challenging for foreigners compared to locals and residents.

To navigate the KYC successfully, preparation is key. Ensure that all information provided is correct and transparent.

{loadmoduleid 1577}

7. How can we help you open a bank account in Hong Kong with ease?

If you need support choosing the right bank or opening the right account for your business at its current stage, contact us. We help you evaluate options, prepare your structure, and open accounts that actually work for your business.

- Recommend the right bank and the right bank account for your needs;

- Support you in opening a reliable, trusted digital bank account or traditional bank account;

- Prepare necessary documents for account opening;

- Schedule an appointment with a Singapore bank representative;

- Monitor and assist in opening personal bank accounts (physical and digital).

8. FAQs about Bank alternatives for UAE companies

The answer is no, traditional banks in Hong Kong require you to have a physical meeting with the banker before opening a bank account.

If your Hong Kong application is not approved, you still have strong alternatives.

One of our most recommended options is Singapore.

Singapore offers a banking system that is highly respected globally, similar to Hong Kong. It provides:

- Strong financial stability;

- Reliable and regulated banking environment;

- Multi-currency accounts;

- International transfer capabilities;

- Business-friendly banking services.

For many entrepreneurs and companies, Singapore banks offer comparable services and support, especially for cross-border business activities.

Most challenges come from compliance and risk assessment.

The process takes between 4-6 weeks or longer for foreigners to see results due to Hong Kong banks’s stringent KYC process.

With over a decade of experience serving as a trusted partner to more than 750 business owners seeking professional development and breakthroughs in the international market, we are an expert strategic corporate service provider helping you incorporate and operate successfully in 10 different countries

Our areas of expertise include:

- Strategic Consulting and Company formation in over 10 different countries worldwide such as Singapore, Hong Kong, the U.S., Australia, Thailand, Malaysia, and offshore destinations like BVI, Belize, Seychelles, and more.

- Account opening for personal and corporate bank accounts, as well as setting up PayPal and Stripe gateqays in countries like Singapore, Hong Kong, and the U.S..

- Tax Consulting and Preparation for SFRS IFRS financial reports, corporate income tax returns, VAT/GST (Value Added Tax/Goods and Services Tax), and more.

- Opreation support:

- Registered adress;

- Foreign consular legalization;

- Trademark and patent protection registration in Singapore and the US;

- Employment Pass application in Singapore and Hong Kong;

- Website design, international SIM number provision;

- DUNS registration.

With over 10 years of experience and a team of experts with 5 to 25 years of experience (international standard certifications) as well as direct partnerships with institutions such as OCBC, UOB, DBS, PayPal, and Stripe, we are proud to offer professional, legal, transparent, sustainable services with no hidden costs.

Global Link Asia Consulting Pte. Ltd. is pleased to announce the publication of the above insightful and informative article on our official website, Global Link Asia Consulting on 03rd April 2026. The copyright for this article is exclusively held by Global Link Asia Consulting Pte. Ltd. Any unauthorized reproduction or distribution of this content without our express written permission is strictly prohibited. We value the protection of our intellectual property and appreciate your cooperation in adhering to these guidelines. Thank you for your continued support of Global Link Asia Consulting Pte. Ltd.